Today the European Commission announced the extension of its deadline for the merger review of Microsoft’s $69 billion acquisition of Activision Blizzard King by 10 working days to April 11, 2023. According to the website of the EC’s Directorate General for Competition (DG COMP), this decision was made under Article 10(3)2 of the EU’s Merger Regulation.

In my interpretation of the statute, the basis must have been a request by the notifying parties:

-

If formal commitments are offered, the deadline is extended by 15 (not 10 as here) working days, and only if such commitments are offered at least 55 working days after the initiation of proceedings. Here, it’s clearly too early for that: the transaction was notified on September 30, and Phase 2 began last week.

-

The second subparagraph of Article 10(3) allows for an extension of up to 20 working days at the request of the notifying parties, provided that such request is made “not later than 15 working days after the initiation of [Phase 2] proceedings.” Also, the commission can always agree on such extension with the parties.

Extensions under the second subparagraph (which are requested by the parties or agreed upon by the Commission and the parties) do not require any formal offer of commitments, nor does anything prevent parties from offering commitments and (previously or subsequently) requesting (or agreeing with the Commission on) an extension.

A few days ago, Microsoft Gaming CEO Phil Spencer restated in the clearest and most specific terms to date that Microsoft is prepared to provide reasonable assurances to Sony regarding the continued availability of Activision’s Call of Duty on the PlayStation. While Microsoft did not offer commitments during Phase 1, the combination of today’s procedural announcement by the Commission and Microsoft’s apparent willingness to find a solution makes me–an app developer who has complained over Apple’s and Google’s app distribution terms–hopeful that we will indeed see a mobile app store by Microsoft that could pose a formidable challenge to Google’s and Apple’s app store monopolies. According to a court filing by Epic Games, Google was afraid of Activision Blizzard King working on an Android app store of its own.

It is my personal opinion that Microsoft-ActivisionBlizzard is a case for unconditional clearance: the issues are numerical (mind-boggling numbers), not legal. Also, the Commission has sometimes cleared mergers not on the basis of formal commitments but public statements that satisfactorily addressed the Commission’s concerns. That is a compromise between unconditional and formally conditional clearance. There are various possible outcomes here. It’s too early to tell what the result will be in this case, but at least for now I just can’t see why the extension of the deadline by 10 working days would be bad news (unless you’re Google and want to renew your $360 million three-year deal with Activision Blizzard King).

Share with other professionals via LinkedIn:

Here’s a quick Ericsson v. Apple update. Ericsson yesterday filed an unopposed motion that surfaced today, narrowing one of the three USITC investigations of Ericsson complaints over Apple from five patents-in-suit to three, and from four patent families to three.

The investigation no. is 337-TA-1300. You can find the five original patents-in-suit here. By way of a motion for partial termination of the investigation, Ericsson drops

-

all asserted claims of U.S. Patent No. 9,705,400 on a “reconfigurable output stage” (a patent that I already identified in late September as a candidate for withdrawal, and even more so when I saw that the Patent Trial and Appeal Board (PTAB) of the United States Patent and Trademark Office (USPTO) had instituted an inter partes review further to a petition by Apple);

-

all asserted claims of U.S. Patent No. 9,853,621 on a “transformer filter arrangement” (which is from the same family as U.S. Patent No. 9,509,273, four claims of which remain in the investigation); and

-

various–but not all–claims from each of the other three patents.

On November 4, Apple had brought a motion for summary determination of non-infringement and/or no technical domestic industry of the ‘400 patent (that part of the motion is now moot) and of no technical domestic industry for the ‘770 patent, which Apple argues Samsung’s devices (Samsung is a key Ericsson licensee) don’t practice, but Ericson continues to assert claims 1,2, and 7 of that patent.

Administrative Law Judge MaryJoan McNamara will preside over an evidentiary hearing (trial) in early January. The most interesting patent-in-suit in that investigation may very well be U.S. Patent No. 7,151,430 on a “method of and inductor layout for reduced VCO [voltage-controlled oscillator] coupling.” Erisson is asserting claims 2-3, 5-8, and 13-18 of that patent, and a subset of those claims (all but claims 14 and 18) in the domestic industry context.

In other Ericsson v. Apple news, Apple can again sell 5G devices in Colombia after an appeals court lifted a preliminary injunction that Ericsson was allowed to enforce for about four months. Most likely, the next Ericsson v. Apple injunction will come down in Germany (in the first half of next year), be it in Mannheim–where a first trial was held earlier this month–or in Munich, where Ericsson is already on the winning track with respect to two patents. However, the last patent spat between those parties led to a settlement at roughly the stage at which the current dispute is as we speak, so it remains to be seen how many decisions will actually have to be handed down.

Share with other professionals via LinkedIn:

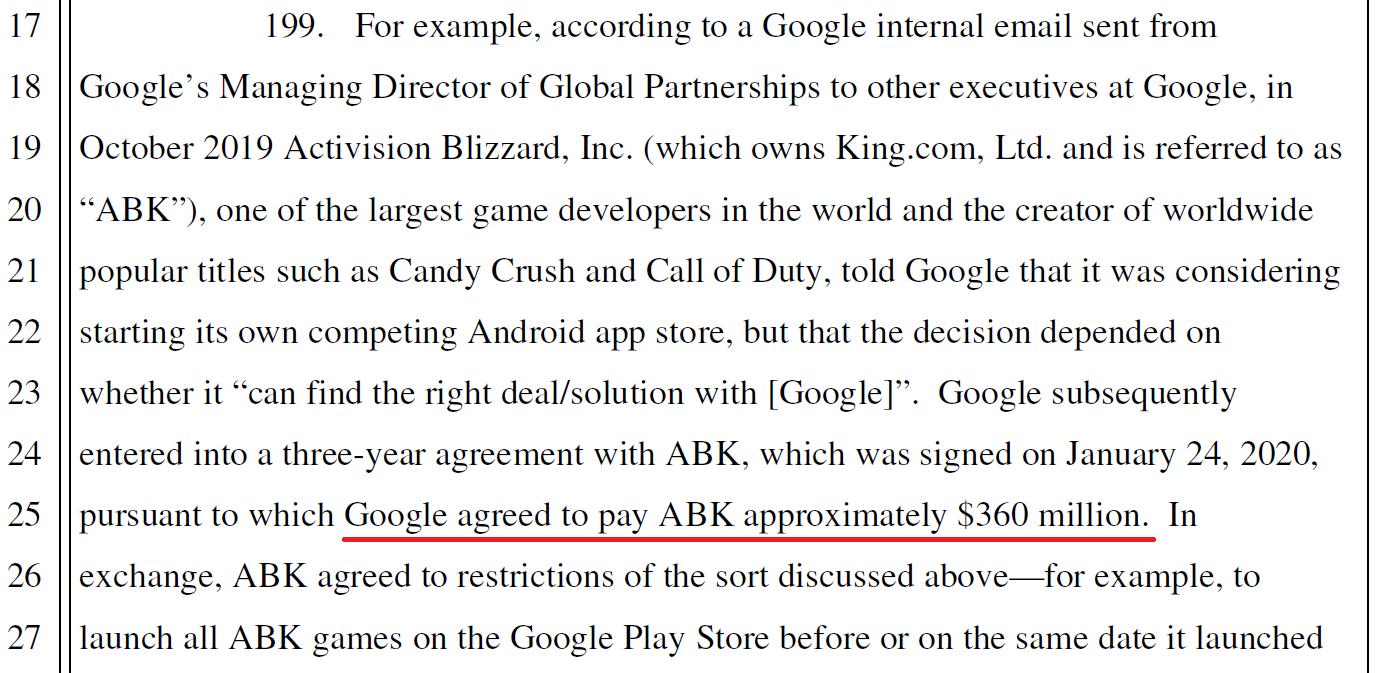

Google fought hard to keep this number a secret–and lost.

The world now knows that in January 2020, Google signed a three-year agreement with Activision Blizzard King (“ABK”), “pursuant to which Google agreed to pay ABK approximately $360 million” in order to dissuade Activision Blizzard from creating its own Android app store. Three-hundred and sixty million dollars for not competing.

First, a screenshot in which I underlined that revelation (click on the image to enlarge):

Second, the complete document:

Exhibit A to Epic Games’ motion to amend its antitrust complaint against Google

That number would be staggering under any circumstances, but it couldn’t have been revealed at a more important point in time: as antitrust authorities in the U.S. (Federal Trade Commission (FTC)), EU (Directorate General for Competition (DG COMP) of the European Commission), and the UK (Competition & Markets Authority (CMA)) have to make their next decisions on Microsoft’s acquisition of Activision Blizzard King. While Sony is the only vocal complainant, Google is also known to have been lobbying behind the scenes.

In a recent filing with the CMA, Microsoft announced its plans to “shift consumers away from the Google Play Store and [Apple] App Store” leveraging Activision Blizzard King’s mobile games. Just this week, Microsoft Gaming CEO Phil Spencer gave an interview to The Verge in which he said in no uncertain terms that Sony’s concerns over the continued availability of Activision’s Call of Duty (CoD) on the PlayStation can be addressed and–as GameSpot summed it up–that the deal is more about Candy Crush (the most popular mobile game ever) than CoD. On other occasions, Mr. Spencer has also talked about the traction that the mobile versions of some of ABK’s other games have.

The fact that Google considered ABK so key to the maintenance of its Android app distribution monopoly as to pay $360 million dollars serves to validate Mr. Spencer’s stated strategic priority regardless of the fact that the recent launch of CoD Modern Warfare II has been wildly successful. Everyone can see now that ABK’s mobile games are indeed key to opening up mobile app distribution. In this case, money–Google’s money–speaks a very clear language.

When the European Commission opened its in-depth investigation of the merger last week, I wrote that “Microsoft’s acquisition of Activision Blizzard King will further the goals of the EU’s Digital Market Act (DMA).” Again, that was on the money. On Google’s money.

In the same post in which I quoted Microsoft’s plans for competing with Apple’s and Google’s mobile app stores (I was first to do so), I also mentioned Epic’s fight for transparency. Google insisted that not only the $360 million figure but also various other facts concerning that deal with Activision Blizzard King remain sealed. Epic would actually have accepted to keep the dollar amount secret, but at least wanted “ABK’s plans to create an alternative game distribution platform, and its changes to those plans as a result of its agreement with Google” to become known, as they “are critical to the public’s understanding of how and why Google’s payments not to compete were unlawful, and how Google has been able to monopolize the markets at issue in these cases.”

Now, surprisingly, even the dollar amount has been revealed. Judge James Donato of the United States District Court for the Northern District of California had entered the following order on Tuesday (November 15):

“The request by plaintiffs Epic and Match to file amended complaints, […], is granted. The amended complaints must be filed by November 29, 2022. The parties are directed to file a joint proposed amended scheduling order by December 13, 2022. The requests to seal the motion to amend briefs are denied for lack of good cause. […] Unredacted versions should be filed by November 22, 2022.”

It often happens in U.S. federal court, and above all in that particular district, that judges insist on transparency. Here, Judge Donato went beyond what Epic was asking for, and it is great that he did.

Here’s a quick recap of the procedural context:

-

On October 7, Epic and Match Group (Tinder) filed a motion to amend their complaints. For Epic, that’s already the second amended complaint; Match joined the case later (only this year), and for them it’s the first amended complaint. The key change is that they allege a per se violation of the Sherman Act through Google’s “Project Hug” (of which the deal with Activision Blizzard King is the most interesting part now, but there were about two dozen deals like that). A per se violation would be deemed unlawful without the court having to analyze any procompetitive justifications (no “rule of reason”).

-

Two weeks later, Google opposed the motion to amend those complaints. I disagreed with Google’s arguments. They claimed a vertical relationship where all that mattered was a horizontal one; and the “prejudice” they alleged they would suffer from the amendments looked to me like something that couldbe offset by the right to conduct some additional discovery (if necessary at all).

-

On November 15, Judge Donato granted the motion, and asked the parties to propose an amended case schedule (by December 13). We may see alternative proposals then.

Furthermore, Judge Donato denied the related sealing motions “for lack of good cause.” This was a win for Epic, even going beyond what they asked for. Epic wants transparency; Google insisted on secrecy, but to no avail.

Earlier today I reported on another interesting decision: all plaintiffs (three dozen U.S. states, Epic, Match, and consumer class-action plaintiffs) want Google sanctioned over the systematic and automatic deletion of company-internal chats, and Judge Donato will hold an evidentiary hearing in mid January before adjudicating the motion.

It’s been quite a week in the mobile app store antitrust arena, which started with the Epic Games v. Apple appellate hearing on Monday (initial commentary and further analysis).

Share with other professionals via LinkedIn:

This is a follow-up to yesterday’s post on why actual numbers of narrowband IoT-related standard-essential patents are hard to come up with, and keyword searches are inherently unreliable in this context. Tim Pohlmann, the founder and CEO of IPlytics, reacted on LinkedIn, first under his personal and then posting the same statement under IPlytics’ corporate account. He “doth protest too much”–and he contradicts himself:

The actual report purports to “paint a robust picture of the NB-IoT landscape” (emphasis added) and to “provide meaningful, actionable insights.” The headline is “Who is winning the IoT SEP race?” (on the website: “Who is leading the IoT SEP race?”) On LinkedIn, however, Mr. Pohlmann wrote the following, which contrasts nicely with his marketing claims:

“Our reports are not published to provide the truth about the winner[s]. We publish reports to show[]case what can be done with the data we provide. We do not care who ranks first[,] second or third.”

IPlytics wants to have it both ways. They make bold claims and promises in public, and their reports have been used not only in licensing negotiations but also by litigants. Once you challenge the methodology and question the results of a particular report, they distance themselves even from its very headline (“Who is winning…”), downgrade the piece to a “showcase,” suddenly discover humility, and place the emphasis on a disclaimer (“our data analysis and report results are limited to the approach of a patent declaration-based keywords search”).

I would recommend to litigants whose adversaries proffer IPlytics reports to show to the court what Mr. Pohlmann publicly stated on LinkedIn in response to my criticism. Toying around with a database isn’t necessarily admissible evidence.

Sadly, the inconsistencies don’t end there. Just two examples in the NB-IoT context, comparing last week’s report to its 2020 predecessor (Who owns patents, SEPs and develops standards for smart home technologies?) in the specific context of NB-IoT portfolio size:

-

Huawei–of which I said yesterday that it and Qualcomm indisputably deserve the two top spots–was not even listed among the top NB-IoT SEP holders in the 2020 report, and now it is (credibly) the number one.

What was IPlytics doing and thinking two years ago? The complete absence of Huawei from the list of leading patent owners should have been more than enough for the report to fail any plausibility check before it was published. IPlytics should have asked themselves whether their methodology was sound given that such an outcome was inexplicable. Instead, they went ahead and published their report anyway. How “robust” and “actionable” is that?

-

For Nokia, Figure 4 of the 2020 report indicated approximately 2,300 patents from 500 patent families. In the 2022 report, however, those numbers are down to approximately 400 patents from 150 patent families (Figure 1). How can Nokia possibly have lost 5 out of 6 assets–and more than 2 out of 3 patent families–during a two-year timespan? Again, how is that “robust” and “actionable” short of a patent cliff of unprecedented proportions in the field of wireless communications technology? And how is it responsible to create such confusion around a key long-term growth area for a publicly traded company like Nokia?

I emailed Mr. Pohlmann before German office hours on Thursday, and received a reply a few hours later: a detailed email that for the most part sidesteps the issue I raised (the above discrepancies between the 2020 and 2022 reports). Only one paragraph really addresses my question, and Mr. Pohlmann (with whose company I signed an NDA a long time ago) authorized publication of his email, so let me quote:

“The smart home report from 2020 used a much simpler approach. Here only TS [technical specifications] that mention NB-IoT and LTE-M were identified to then connect this given list [of] TS to declared patents. So this report uses a keyword search in TS documents that have declared patents associated. The data approach of both reports are quite different. Also I must say that the number of declared patents has very much increased since July 2020.”

The “much simpler approach” in 2020 did not dissuade IPlytics from publishing it (and declaring “winners”) at any rate. If they say in 2022 that they’ve improved since the 2020 report, what will they tell us in 2024?

The last sentence about a massive increase in the number of declared patents (by the way, we’re talking about subsets of the 4G standard, which is already quite mature by now) still doesn’t explain why they published a list in 2020 (instead of immediately identifying an issue) without Huawei–the actual number one–among the top 10 patent owners. Mr. Pohlmann is a frequent speaker at SEP conferences, which in addition to his own company’s patent database provides him with plenty of opportunity to get a feel for the market.

It is unfortunate that it is so hard to determine portfolio sizes in the narrowband IoT context. There are some companies who may only have a 1% or 2% share of all 4G/LTE SEPs, but their research may be disproportionately focused on parts of the standard that are relevant to its narrowband subsets (LTE-M and NB-IoT). Someone who is an average-sized fish in the larger pond may be a bigger fish in the smaller pond. Someone who filed for patents before those narrowband subsets were defined will not have used certain keywords in the claims or specification of a given patent application, but it may later read on NB-IoT and/or LTE-M anyway (false negatives under a keyword-based approach), while someone else may just have thrown in some keywords at a later stage, which doesn’t guarantee that a given patent actually maps to the relevant specification of the standard.

IPlytics should be lower-key in its PR and marketing communications. That will lead to greater consistency. It’s always better to underpromise and overdeliver, especially when there is the possibility of those reports being used in litigation or relied upon by policy makers and regulators.

Share with other professionals via LinkedIn:

While this doesn’t necessarily mean that Google will be sanctioned for the systematic deletion of company-internal chats, the plaintiffs in the Google Play antitrust case in the Northern District of California have achieved a potential breakthrough:

Less than a week after the plaintiffs filed their reply brief in support of their motion for discovery sanctions, Judge James Donato of the United States District Court for the Northern District of California has determined that this matter is worthy of further scrutiny. An evidentiary hearing that is anticipated to “go for no more than 3 hours” will be held on January 10, 11, or 12. It’s like a discovery-specific minitrial (in court, not arbitration where the term is used more frequently).

Judge Donato’s order lays out the agenda as follows:

“In addition to anything else the parties would like to present at the hearing, the Court anticipates testimony by Google witnesses about the use and operation of the electronic chat system, including storage and deletion policies, guidelines for chat content, and examples of typical chat communications. Google will present this information through direct examinations of the witnesses, and plaintiffs will cross-examine. The Court will hear argument on the discovery dispute immediately after the close of evidence.” (emphasis added)

In my commentary on the reply brief I said it was difficult to form an opinion on the merits of the motion from the outside: some key passages (quoting testimony) were sealed. What I deduce from the order is that what Judge Donato has seen is serious enough that evidence must be taken. And it appears to be too relevant for the court to just deny the motion on the papers. At the same time, the plaintiffs’ preferred sanction, which would be an adverse inference–not like a procedural equivalent of the death penalty, but incisive and impactful. Before the court could do that, Google is given another chance to justify its conduct. But above all, it’s a chance for three dozen U.S. states, Epic Games, Match Group, and the consumer class-action plaintiffs to argue that an adverse inference is warranted (or, as a fallback position, a curative instruction).

If not for the Epic Games v. Apple appellate hearing on my Monday (initial commentary considering a remand the most likely outcome; and a follow-up explaining why “failure of proof” is a hurdle that I believe Epic can overcome), this decision to hold an evidentiary hearing over the systematic and automatic deletion of Google Chats would be the most significant development in the App Store antitrust lawsuits this week.

Share with other professionals via LinkedIn:

For about four months, Ericsson was enforcing against Apple a preliminary injunction by a Colombian court over a 5G standard-essential patent. Apple asked the United States District Court for the Eastern District of Texas to interfere, but Judge Rodney Gilstrap declined the invitation. In Colombia, invoked the Universal Declaration of Human Rights, but the PI was deemed constitutional.

On Tuesday, an appeals court lifted the PI and Apple is now–until another injunction comes down, such as after a full trial–again able to sell 5G-compatible devices in Colombia, a market in which Apple generates only about 0.2% of its worldwide sales. The Sala Civil del Tribunal Superior del Distrito Judicial de Bogotá D.C., (Superior Court for the Judicial District, Civil Law Division) decided to vacate the injunction and to deny the “preliminary relief requested by Telefonaktiebolaget LM Ericsson”:

This doesn’t mean that Colombian users will actually get to enjoy 5G bandwidths: in the South American country, the network infrastructure isn’t 5G-capable yet. But the more recent iPhone and cellular iPad generations all come with 5G, and Apple wasn’t going to make a 4G iPhone 14 just for Colombia, which is why Apple couldn’t launch the iPhone 14 in Colombia at the time it did elsewhere. Now it’s just a matter of time until the iPhone 14 will show up in Colombian retail stores–and Apple will take orders via its Colombian online store (which by the time I published this article still said that Apple couldn’t offer 5G devices in Colombia due to a court order). This may take a few weeks due to manufacturing bottlenecks.

Other gadgets that Apple can now sell in Colombia–and which were available there until the PI came down in the summer–include the iPhone 12, iPhone 13, and recent generations of the iPad.

The court decided not to award any fees as the lifted injunction was properly based on the representations made by Ericsson at the time without relying on the materials subsequently presented by Apple Colombia.

The order–signed by Judge Jorge Eduardo Ferreira Vargas–explains that on appeal there was a different procedural situation and the appeals court now has the benefit of Apple’s additional arguments according to which it believes it is no longer reasonable–though it was at the time–to presume that Apple infringes the asserted patent claim (claim 13 of Colombian patent no. 36031). For example, Apple argued that there were “significant differences” between the claim language and the relevant part of the 5G standard. Apple filed a sworn declaration by an expert (after the PI had been granted). Apple also argued that the patent is invalid.

The fact that the general public doesn’t have access to 5G in Colombia was not considered relevant, as a PI can also serve to prevent future acts of infringement.

While the appeals court does not generally rule out that preliminary injunctions over Colombian patents could be granted even on an ex parte basis (without hearing the defendant), it holds that it is premature to presume at this stage that the patent claim in question is indeed infringed. So this was a very case-specific determination, and Ericsson can still prevail in the main proceedings.

Let’s put this into context. With the Colombian PI having been lifted, there isn’t currently any court decision that Ericsson can enforce against Apple or the other way round. However, various Ericsson v. Apple rulings will come down in the early part of next year (unless the parties settle before):

In September, the Munich I Regional Court (the world’s #1 patent injunction venue) held first hearings (remotely comparable to Markman hearings in the U.S.) in a SEP case–after which the court denied Apple’s motion to dismiss–and a non-SEP. In both cases, the Munich court is inclined to hold Apple to infringe Ericsson’s patents. On December 21, the Munich court will hold a FRAND hearing.

Last week, the Mannheim Regional Court held the first of a series of Ericsson v. Apple SEP trials. It’s very likely that Ericsson will prevail on the technical merits, though the court promised to take another close look at Ericsson’s arguments for a stay. The courtroom was sealed for the FRAND part, so I don’t know what was said, but suffice it to say that Apple would be the first defendant in Mannheim (and Munich) in the post-Sisvel v. Haier era to prevail on a FRAND defense.

A week ago, the ITC conducted the first of three evidentiary hearings (i.e., trials) in its investigations of Ericsson’s three complaints against Apple. Apple’s countercomplaint will go to trial next month; Ericsson’s other two complaints will be tried early next year. The ITC is a “patent graveyard” where complainants have a low hit rate (this also applied to Apple when it was suing Android device makers, with the exception of a case against Samsung that turned out useless nonetheless because Samsung simply worked around the asserted patents). But with three investigations ongoing, chances are that Ericsson will something sooner or later.

Cases are pending in other jurisdictions as well, such as in the UK. Also, Ericsson filed various actions in Colombia, including multiple preliminary injunction requests, and the appeals court’s order lifting the preliminary injunction does not prejudge the overall outcome there.

The big question I’ve been asking myself for many months is whether the Ericsson v. Apple FRAND trial in the Eastern District of Texas–which is scheduled to begin on December 5–will actually take place or whether the parties will settle before. It would be the most logical settlement point in that dispute for at least the next six months.

Share with other professionals via LinkedIn:

The Internet of Things (IoT) is a tremendous growth area in multiple respects: for product makers, for standard-essential patent (SEP) holders, and for patent analytics companies looking to acquire new categories of customers. But in the midst of a gold rush, not all that glitters is really gold.

Last week there were two IoT SEP-related announcements: Sisvel’s new narrowband IoT pool, which started with 20 licensors, most notably also Ericsson; and just one day earlier, IPlytics released a report on who is supposedly winning the IoT SEP race. As an IP and antitrust commentator, I wish to help my readers avoid being misled. That’s why I criticized a ranking of German patent litigation firms last month, and suffice it to say I received a lot of positive feedback from people who appreciated it. And there are serious issues with that IPlytics report, which I believe someone has to call out.

Prior to this one, I publicly criticized IPlytics only once, and that was when Tim Pohlmann interviewed the president of an Apple astroturfing operation claiming to represent small app developers and IoT companies while actually working against the interests of small innovators, especially in the App Store antitrust context. When that interview took place, there was enough information out there already to know that ACT is not a legitimate representative of whom the claim to speak for, and IPlytics should (or must) have known that.

Now IPlytics has been acquired by RELX (congratulations!), a company known for such services as LexisNexis. I have no problem with RELX, and I have no position at this stage on whether WIRED is right that RELX’s practices represent a threat to data privacy.

That recent IPlytics report on IoT patent holdings is nothing that decision makers, whether in the public sector (such as competition enforcers and policy makers) or in companies (patent holders, pool administrators, or implementers), should rely on. I have problems with its methodology and with some of the results.

If it wasn’t free, I’d have to say: caveat emptor!

First, the methodology makes it a clear Daubert case (those familiar with U.S. litigation know what I mean, and the others can figure).

The report mentions a “keyword approach” three times. On the penultimate page, there is a disclaimer:

“We used a keyword approach without additional filters for the active or granted status of a patent or patent family. We want to highlight that other keywords or additional selected filters might result in other ranking positions and shares. Further, we refrain from making assessments of the technical relevance of patent portfolios.”

A “keyword approach” cannot make up for a problem facing anyone (not just IPlytics) who will undertake to evaluate the narrowband IoT patent space: there are no databases of NB-IoT- or LTE-M-specific declarations. The reason being that NB-IoT and LTE-M are simply true subsets of the wider 4G/LTE standard, and that’s where the declarations and concomitant FRAND pledges were made. Those narrowband standard-setting efforts started when 4G/LTE was already far along, and what they did was to select those parts of LTE that they deemed suitable to task.

Keywords are a poor indicator, and actually they are no indicator when many patents were filed before it was possible to know or even just predict the relevant keywords. Many 4G/LTE patents read on narrowband IoT, but when the applications were drafted, the keywords simply weren’t floating around yet.

The sad truth is that one would have to get down almost to the level of claim charts to really find out who owns how many narrowband IoT SEPs. That’s obviously not going to happen.

Second, there are some implausible results. And some of those implausible results are plausibly attributable to the methodology issues I just outlined.

I don’t have a plausibility problem with Huawei and Qualcomm coming out on top here. Those two companies have powerful portfolios and long-standing strategic interests related to IoT. It’s hard to think of any wireless technology where they wouldn’t be very strong. My problems are mostly at the level right below Huawei and Qualcomm:

I would normally assume that companies like Ericsson, Nokia, Samsung, and LG are roughly on an equal footing (Ericsson probably being the number one among them)–to give you a ballpark figure, I would expect each of them to hold around 10% of the relevant patents. Those are companies that clearly have not only a general interest in IoT but also participate quite actively in the related standard-setting. But in IPlytics’ narrowband IoT ranking, Nokia is roughly at a level with a company like Lenovo, which has a rather different focus and business model.

Below companies like Ericsson and Nokia, I would see players like Sony and NTT DoCoMo, yet they presumably own more relevant patents than a number of companies listed ahead of them.

Maybe IPlytics did its best and it’s not good enough (yet). So what are the alternatives?

The first alternative in a context like this is simply the Socratic approach. In his Apology, Greek philosopher Plato praised the key quality in Socrates not to think he knows what he doesn’t know. “I know that I know nothing.”

It would be terrific to have a set of numbers that would enable us to get an idea of what the licensing costs for the full stack might be. That would enable top-down royalty determinations, which are so very popular. But we may have to live with the fact that, at least at this stage, we just don’t have the data at hand for that. And when data is unreliable, it’s better to just accept that fact. Things get worse–not better–if we act in defiance of that realization.

There are bogus medications for incurable diseases. They raise false hopes and have adverse effects–as do unreliable rankings, even those produced with the best intentions.

I wouldn’t underestimate the ability of the market to figure out solutions and royalty rates, especially in narrowband IoT, where different standards are competing with each other for “design wins.”

And I would strongly recommend to use common sense. While one can’t assume that companies’ contributions to a standard-setting process always correlate to a given player’s portfolio strength, we should at least look at who really participated in standardization and take that into account, as we all know that those who sit at the standard-setting table will also ensure that some of their technologies are included and will strategically file patents so they read on the relevant standard.

Is more transparency needed in the narrowband IoT context? Absolutely. It should be a priority for the industry to come up with something better, ideally in 2023.

To be clear, I am not taking a position here on any other IPlytics report than the one I specifically mentioned, nor on their raw data or anything else they offer.

Share with other professionals via LinkedIn:

- Coinsmart. Europe’s Best Bitcoin and Crypto Exchange.Click Here

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: http://www.fosspatents.com/