The average cost of a data breach reached a record high of $4.35 million in 2022, and many experts estimate that the average cost of information leakage could reach $5 million in 2023.

Need more proof of the benefits of reliable information protection technologies for financial software?

In this article, we’ll look at key payment processing regulations, strategies to keep up with them, and a FinTech solution to meet the data management regulations.

Table of contents

Payment processing regulations basics

Payment processing refers to the entire system of handling financial transactions, including recording, verifying, and approving payments between a buyer and a seller. It includes various steps such as capturing payment information, transmitting it securely, and processing the transaction.

Meeting new regulations, in the context of payment processing, means adherence to the relevant laws, regulations, and industry standards for financial transactions.

This procedure is important for several reasons.

First and foremost, it ensures the security and integrity of financial transactions and protects both businesses and consumers from fraudulent activity.

Compliance also helps maintain transparency and accountability in the financial system and prevents money laundering, terrorist financing, and other illegal activities.

In addition, this process builds users confidence, improves a company’s reputation, and mitigates the risk of penalties, fines, and legal consequences.

The regulatory environment for payment processing is complex and can be difficult to navigate.

There are numerous regulations that payment processing businesses must comply with, including the Payment Card Industry Data Security Standard (PCI DSS), the Second Payment Services Directive (PSD2) and the General Data Protection Regulation (GDPR). Each of these regulations has specific requirements that businesses must adhere to.

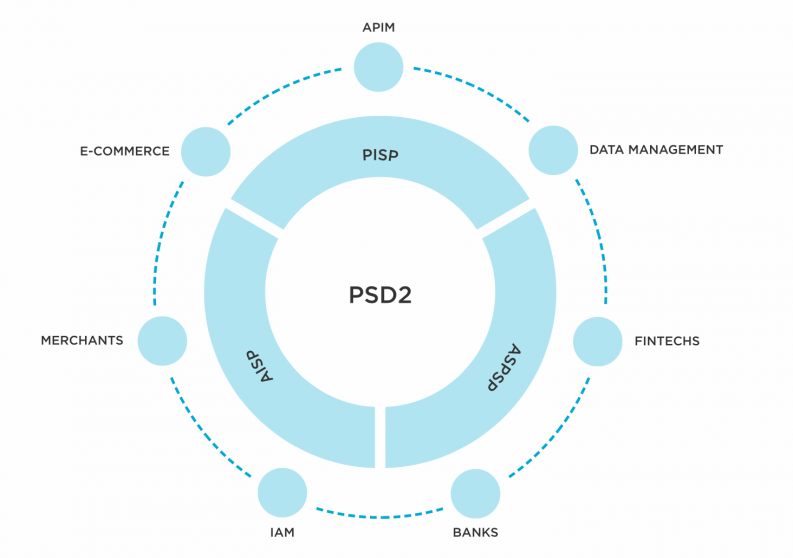

PSD2

What is PSD2? PSD2 stands for the Second Payment Services Directive. It is a European Union directive that regulates payment services within the EU and the European Economic Area. PSD2 was introduced to promote competition, innovation, and security in the payment industry while enhancing consumer protection.

The main objectives of PSD2 are:

- Increased security

PSD2 mandates stronger authentication measures for electronic payments to reduce the risk of fraud and unauthorized access. It introduces the concept of Strong Customer Authentication (SCA), which requires customers to provide two or more forms of authentication when initiating electronic payments.

- Open banking and third-party access

PSD2 promotes open banking by requiring banks to give authorized third-party payment service providers (TPPs) access to their customers’ account data, subject to their consent. This allows TPPs to initiate payments and access payments data, which promotes competition and innovation in the payments industry.

- Consumer protection

PSD2 strengthens consumer rights by imposing strict liability rules on payment service providers for unauthorized or fraudulent transactions. It also enhances transparency by requiring detailed information on transaction fees and charges.

- Harmonization of regulations

PSD2 aims to harmonize payment rules across the EU and EEA to create a level playing field for payment service providers and facilitate cross-border transactions.

The technology required for PSD2

The directive requires that payment service providers expose open APIs, enabling secure access to bank accounts and information through third-party providers. There are three primary categories of these providers.

- Account Information Service Providers (AISPs). They have access to sensitive data, allowing them to analyze spending patterns and gain valuable business insights.

- Payment Initiation Service Providers (PISPs). These service providers facilitate transactions for both consumers and FinTech companies.

- Account Servicing Payment Service Providers (ASPSPs). These are institutions, such as banks, building societies, wealth management companies, and investment firms, that offer payment accounts with online access.

Source: Tibco

These institutions process sensitive data privacy, including card information, bank account information, full names, and government identification numbers. Consequently, institutions that comply with PSD2 must also comply with GDPR regulations to ensure the protection of personal data.

Consequently, PSD2 has had a significant impact on the financial services industry, encouraging the development of new payment solutions such as mobile payments and peer-to-peer transfers. It has also paved the way for innovative services from fintech companies and led to increased competition between traditional banks and new entrants.

PCI DSS

PCI DSS stands for Payment Card Industry Data Security Standard. This is a set of security standards developed by major payment card manufacturers, including Visa, Mastercard, American Express, Discover, and JCB International.

The primary goal of PCI DSS is to protect cardholder info and prevent unauthorized access, fraud and data breaches. Meeting the PCI DSS rules is mandatory for any organization that accepts, processes, stores or transmits payment card information.

PCI DSS provides the comprehensive regulatory frameworks for businesses that process payment card data to ensure the secure processing, storage, and transmission of cardholder data.

What is PCI DSS?

[embedded content]

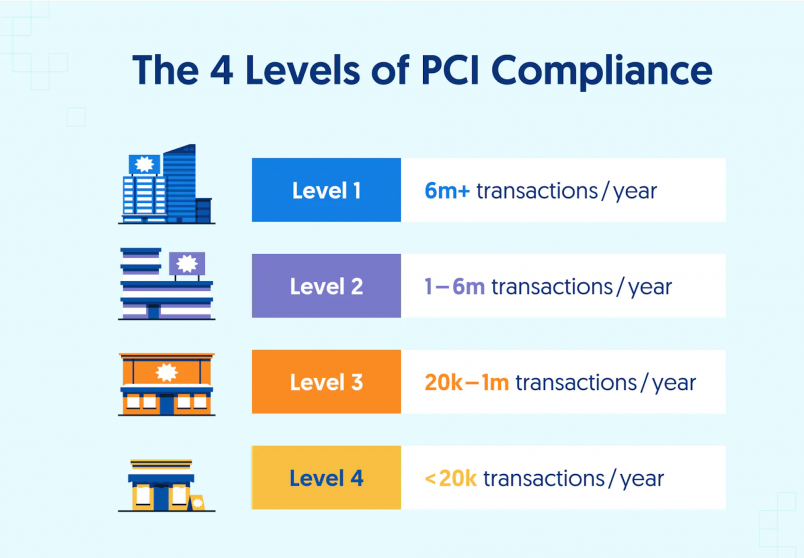

The application of the requirements of PCI DSS depends on the nature of the organization and the volume of transactions it processes. There are four levels of compliance with PCI DSS, corresponding to different merchant categories.

- Level 1. Applicable to merchants processing over 6 million card transactions annually.

- Level 2. Applies to merchants processing between 1 and 6 million transactions per year.

- Level 3. It is required for merchants handling transactions amount ranging from 20 thousand to 1 million per year.

- Level 4. It is required for merchants processing up to 20 thousand transactions annually.

The requirements for PCI regulatory requirements vary for each level, with Level 4 being the least stringent and Level 1 being the most stringent.

Source: Secure Frame

The cost of non-compliance

The consequences of non-compliance with PCI DSS go beyond financial losses to include damage to reputation.

- Fines and penalties are possible consequences of violating PCI DSS, as card networks may impose them. The amount of fines depends on the severity of the non-compliance and the frequency of violations and can range from $5,000 to $100,000 depending on the specific circumstances.

- Non-compliant businesses may face additional financial burdens in the form of increased transaction fees charged by card issuers. These additional fees can begin to accumulate and directly impact the overall business profitability.

- Non-compliance with PCI DSS can also lead to legal action and lawsuits from affected customers or financial institutions. The resulting legal costs may include various expenses such as attorney’s fees, settlements and other legal costs.

Therefore, it is important for businesses to comply with PCI DSS to protect the cardholder data privacy they handle, maintain user trust, and mitigate the risk of security breaches and financial losses.

GDPR

GDPR stands for the General Data Protection Regulation. It is a comprehensive regulator introduced by the European Union (EU) in May 2018. The GDPR replaces the 1995 Data Protection Directive and aims to harmonize and strengthen system protection laws in EU member states.

The main objectives of the GDPR are: as follows.

Improved protection of personal data

The GDPR places great emphasis on the protection of personal info. It defines personal data in the broadest sense and requires organizations to obtain clear and informed consent from individuals before collecting, processing or storing their personal info.

Extended rights for individuals

The General Data Protection Regulation grants individuals more control over their personal data. It gives individuals rights such as the right to access their info, the right to correct inaccurate data, the right to be forgotten, and the right to data portability.

Accountability and transparency

The General Data Protection Regulation requires organizations to demonstrate accountability and transparency in their processing activities. It requires organizations to implement appropriate info protection measures, conduct data protection impact assessments for high-risk activities, and keep records of their processing activities.

Cross-border data transfers

The General Data Protection Regulation establishes a framework for lawful transfers of personal details outside the EU. It requires companies to implement appropriate safeguards when transferring personal info to countries or organizations that do not provide an adequate level of data protection.

Stricter enforcement and sanctions

The General Data Protection Regulation introduces stricter enforcement mechanisms and significantly higher penalties for breaches. Companies can be fined up to 4% of their annual global turnover or €20 million, whichever is greater, for serious breaches of the regulation.

5 key steps for reaching GDPR compliance

[embedded content]

The General Data Protection Regulation applies to any businesses that processes personal details of individuals residing in the EU, regardless of the organization’s location. It has global implications, as many organizations outside the EU must comply with the requirements of the GDPR to ensure the protection of EU citizens’ personal info.

KYC and AML procedures

Payment processing requirements encompasses a range of practices and regulations designed to ensure the integrity and security of financial transactions. Among the key components of payment processing compliance are Know Your Customer (KYC) and Anti-Money Laundering (AML) regulators.

KYC procedures involve collecting and verifying customer information to establish their identity, assess potential risks, and ensure compliance with regulatory requirements. This includes gathering personal details, such as name, address, date of birth, and government-issued identification documents.

Three components of KYC include the customer identification program (CIP), customer due diligence (CDD), and enhanced due diligence (EDD).

Customer identification program

The Customer identification program (CIP) mandates that financial institutions acquire four essential pieces of user information, which encompass the customer’s name, date of birth, address, and identification number.

Customer due diligence

CDD is a process of collecting all of a customer’s info to verify their identity and assess their risk profile for suspicious account activity.

Enhanced due diligence

Enhanced due diligence is applied to users who are at higher risk of infiltration, terrorist financing, or money laundering and often require additional information to be obtained.

AML measures are designed to detect and prevent money laundering and the financing of illegal activities through the financial system. These measures require organizations to establish internal controls, conduct thorough due diligence on users and transactions, and monitor for suspicious activities in banking industry. By implementing AML practices, businesses contribute to the overall efforts to combat financial crime and maintain the integrity of the financial system.

Effective implementation of KYC and AML regulators not only helps organizations comply with regulatory obligations but also safeguards their reputation, reduces financial risks, and protects users from potential harm. By prioritizing payment processing laws, businesses demonstrate their commitment to maintaining a secure and trustworthy financial ecosystem.

Strategies for navigating the regulatory landscape

Keeping up with the changes

It is critical to actively monitor and stay abreast of regulatory changes relevant to your industry. Review and analyze updates regularly to ensure compliance with the latest requirements. For example, you can follow regulatory websites or join a professional association.

Automate reporting and documentation

Develop a robust compliance program tailored to your organization’s specific needs. Leverage technology solutions such as Compliance 360, MetricStream or ZenGRC that are designed to streamline the processes. These software and tools can automate tasks, track these activities and generate reports to increase efficiency and accuracy.

Outsource compliance tasks

If the complexity of compliance processes becomes too great, consider outsourcing certain tasks to specialized companies or consultants. They can provide expertise, guidance and support so your company can effectively meet the policy requirement.

By implementing these strategies, companies can better navigate the regulatory landscape, reduce the risks and foster a culture of compliance within their organizations.

How can payment processing software simplify the compliance process?

Regulatory compliance can be a stumbling block for many payment processing companies around the world, but SDK.finance handles this via a FinTech hybrid-cloud solution to help meet the data management regulations .

The practice of not allowing the use of cloud services to store user information outside of a country’s borders is commonly referred to as data localization. This is done primarily for security, privacy, and regulatory reasons, as it allows the government to maintain control over the data and enforce local laws and regulations regarding information protection. For example, Saudi Arabia’s decision to restrict the use of cloud services for storing user info outside the country’s borders aligns with the concept of data localization.

There are no location-based restrictions on the use of SDK.finance‘s payments software. The primary databases are under your team’s control, while SDK.finance hosts and maintains the back-end application on AWS or another cloud service provider. As a result, you can meet policy requirement related to the management and storage of sensitive info.

Our white-label software serves as the digital foundation for building e-wallets, neobanks, payment acceptance and money transfer systems. With more than 400 API endpoints, the SDK.finance system streamlines the development of a wide range of digital banking and payment products, as well as the creation of custom integrations with third-party providers.

Conclusion

By prioritizing payment processing compliance issues and implementing effective strategies, organizations can protect sensitive information, ensure regulations, build customer trust, and ensure their long-term success in the evolving digital payments landscape.

SDK.finance‘s payment software can help with compliance with all data localization regulations via a hybrid cloud solution. Contact us to discuss which FinTech software option is best for you.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoAiStream. Web3 Data Intelligence. Knowledge Amplified. Access Here.

- Minting the Future w Adryenn Ashley. Access Here.

- Buy and Sell Shares in PRE-IPO Companies with PREIPO®. Access Here.

- Source: https://sdk.finance/payment-processing-and-compliance-navigating-the-regulatory-landscape/