Welcome to the future of financial services, where innovation and collaboration create a seamless banking experience – the era of banking as a platform. But what exactly is platform banking, and how does it differ from a traditional one?

In this article, we will delve into the essence of the platform banking, uncovering its core principles, key features, and transformative impact on the financial industry.

Table of contents

Understanding what is platform banking

Platform banking goes beyond the traditional model and transforms banks into dynamic ecosystems where different financial services seamlessly merge. It promotes a shift toward customer-centricity that focuses on understanding and meeting individual needs and preferences.

What is platform banking?

Platform banking, also known as banking as a service (BaaS) or banking platform as a service, is an innovative approach to banking that leverages technology, APIs (application programming interfaces), and open architecture to create a connected ecosystem of financial services.

In this model, a bank transforms into a platform that offers a wide range of financial products and services through a unified interface and collaborates with various fintech companies, developers, and partners.

The concept of banking platform as a service goes beyond traditional banking services and aims to provide customers with a seamless, integrated experience that meets their diverse financial needs. It enables financial institutions to expand their offerings beyond core banking services and bring together various value-added services such as payments, lending, investments, and more under one roof.

Watch this video to learn more about the bank as a platform system:

[embedded content]

Through APIs, platform banking facilitates secure and controlled access to a bank’s data and functionality and enables third-party developers to integrate their applications and services with the bank’s platform.

This integration fosters collaboration between banks and fintech companies, leading to greater innovation, customer-centric solutions, and a competitive advantage in the financial services market.

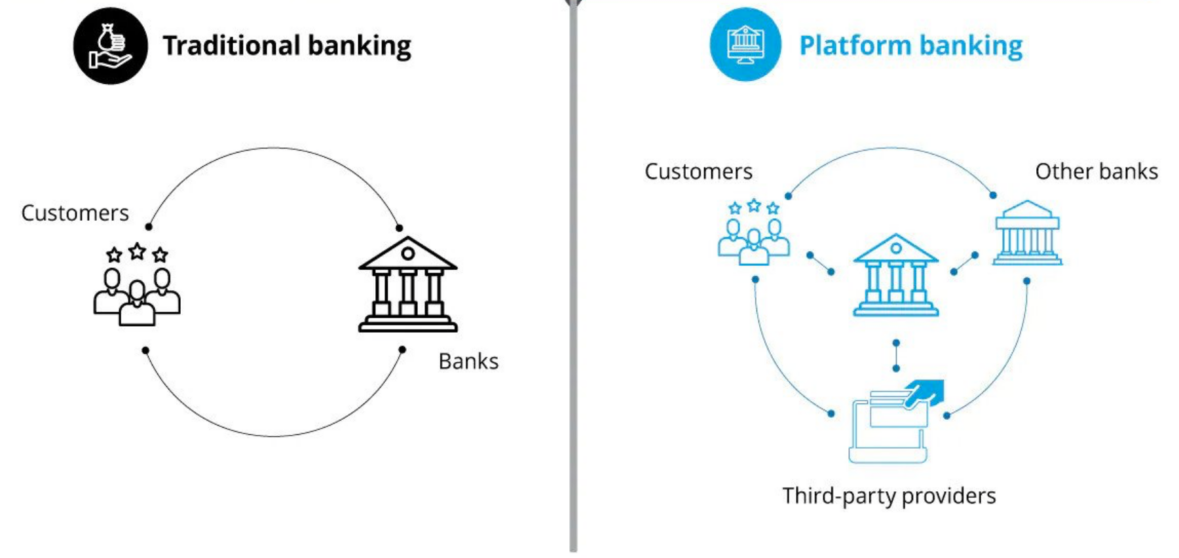

Traditional banking vs platform banking

Traditional banking and bank as a platform are two different systems in the financial industry, each with its own characteristics, advantages, and challenges.

Traditional banking involves the provision of basic financial services, such as deposit-taking, lending, and other related services, by banks and financial institutions directly to their customers.

In traditional banking, customers deal with physical bank branches. These often have well-established branches and may also offer services through ATMs and online banking platforms.

The difference between traditional and banking platform as a service

Source: Sitech

While traditional banking was the dominant model for many years, the rise of digital technologies and changing customer preferences have driven the evolution of banking toward more innovative and customer-centric models, such as platform banking.

Bank as a platform is an innovative and transformative digital marketplace, seamlessly operated via user-friendly apps or state-of-the-art software and owned by either a traditional bank or a non-bank.

This platform goes beyond traditional banking to offer a wide range of banking and non-banking services, all conveniently accessible in one integrated space. With a focus on customer-centricity and technological advancement, the banking platform as a service redefines the way financial services are delivered and creates a truly connected and personalized banking experience for users.

The key differences between traditional and platform banking are explained below.

| Aspect | Traditional banking | Platform banking |

| Business model | Vertical business model | Collaborative business model |

| Customer experience | Limited offerings from the bank directly | A wider range of specialized services from third-party partners |

| Innovation and flexibility | Limited adoption of new technologies and innovations | Embraces innovation and agility through collaborations with fintech |

| Financial inclusion | May struggle to cater to underserved populations | Fosters financial inclusion through partnerships with fintech |

| Revenue streams | Primarily from core banking products | Diversified revenue streams through third-party collaborations |

| Competition and collaboration | Competes with other banks and financial institutions | Encourages collaboration with fintech startups and industry players |

Platform banking vs banking as a service

Platform banking creates a unified ecosystem of diverse financial and non-financial services, while Banking as a Service enables third-party companies to offer banking services through their applications or platforms by leveraging existing banking infrastructure.

The main differences between banking as a service and platform banking are explained below.

| Aspect | Platform banking | Banking as a service (BaaS) |

| Definition | A digital marketplace offering diverse financial and non-financial services through a unified interface, collaborating with third-party partners. | Banks provide their banking infrastructure and services to third-party companies for integration into their own applications. |

| Scope of services | Offers a wide range of financial and non-financial products, such as payments, lending, investments, insurance, etc. | Focuses specifically on core banking functionalities, like account creation, transaction processing, card issuance, and payment processing. |

| Ownership | Operated and owned by either traditional banks or non-bank entities. | Provided by banks or financial institutions who own and maintain the banking infrastructure and APIs. |

| Integration approach | Various services from multiple third-party providers are integrated into a single platform. | Third-party companies integrate the provided banking services into their applications or platforms using APIs. |

| Target audience | Caters to end customers seeking a comprehensive and integrated banking experience. | Targets companies and businesses looking to enhance their product offerings by integrating banking services into their applications. |

| Key focus | Creating a holistic and customer-centric banking experience through a diverse ecosystem of services. | Enabling third-party companies to offer banking features to their customers without building the infrastructure themselves. |

| Application scope | Extends beyond core banking services to value-added financial and non-financial services. | Focused on core banking functionalities to enhance the offerings of third-party applications. |

| Example use case | A bank transforming into a digital marketplace offering banking and non-banking services through a unified interface. | A fintech company integrating payment processing and account creation services from a bank into its mobile app. |

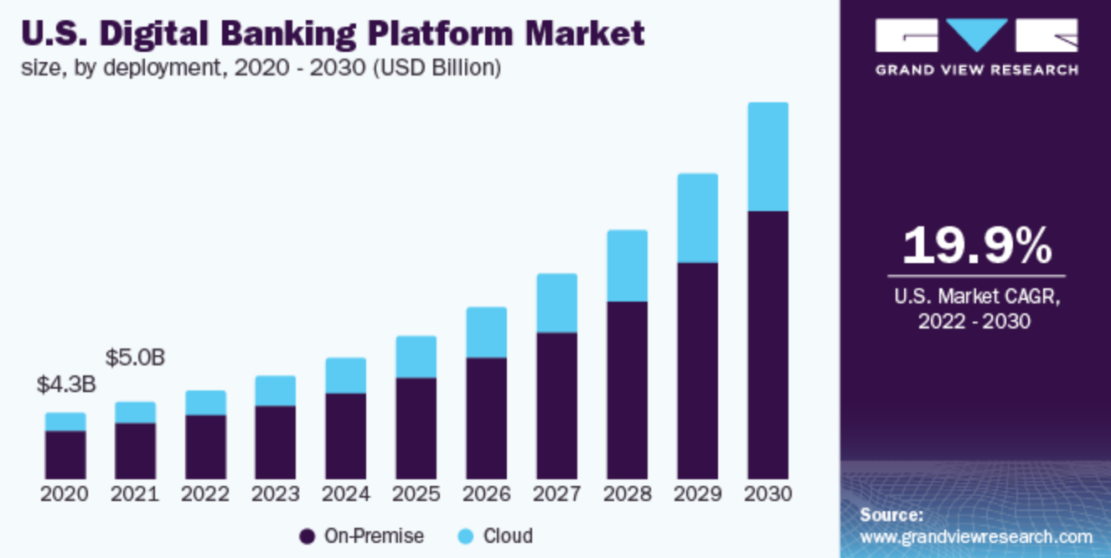

The rise of platform banking

The rapid digitization of the financial sector, changing customer expectations, and the explosion of fintech startups have driven the adoption of banking-as-a-service platforms.

In a connected world, consumers demand more than transactions; they crave seamless, personalized experiences – a demand that banking platforms are enthusiastically meeting.

According to a report by Grand View Research, the global digital banking platform market is expected to grow at a CAGR of 20.5% from 2022 to 2030.

Source: Grand View Research

One such success story is the transformation of XYZ Bank into a “banking platform” by opening its APIs to third-party developers and entering into strategic partnerships. As a result, XYZ Bank saw an increase in its customer base, successfully entered new markets, and ultimately increased its profits.

The impact of the banking platform has been nothing short of revolutionary. Traditional banks are now forced to innovate, partner with fintech startups, and redesign their offerings. This disruption fosters healthy competition that ultimately benefits consumers through a wealth of innovative services and competitive pricing.

Benefits of platform banking

Platform banking offers numerous benefits that are revolutionizing the way financial services are delivered and experienced. Let’s take a look at the key benefits that make bank as a platform a game-changer in the financial industry:

Enhanced customer experience

Platform banking puts the customer at the center of the financial ecosystem. By providing a single interface to access a wide range of financial services, customers enjoy a seamless and personalized experience. The platform’s data-driven insights enable tailored recommendations and solutions that ensure customers’ needs are met efficiently and effectively.

Improved financial accessibility

Platform banking opens the doors to financial services for underserved and unbanked populations. By partnering with fintech companies that specialize in niche areas such as microfinance or digital wallets, banks can offer targeted solutions for specific customer segments to promote financial inclusion.

Diversified revenue streams for FinTech companies

Through collaborations and partnerships, banks can expand their service offerings beyond traditional banking products. By integrating third-party fintech services, banks can create new revenue streams and offer a broader range of solutions to their customers. For fintech companies, platform banking provides access to a larger customer base and the resources of established financial institutions.

Payment Acceptance Software

Affordable software to base a payment processing product on top

Cost-effective solution

Platform banking can be a cost-effective approach for banks. By leveraging the expertise of external partners, banks can avoid the costs associated with developing all services in-house. This cost efficiency leads to better pricing for customers and a competitive advantage in the marketplace.

Increased scalability and flexibility

The modular architecture of platform banking enables scalability and adaptability. Banks can add or remove services based on market needs and customer preferences. This flexibility ensures that platform banking remains relevant and responsive to changing trends and customer needs.

With their numerous benefits, banking as-a platforms are reshaping the future of financial services, driving positive change and providing convenience and accessibility to customers worldwide.

Key challenges and risks of platform banking

While platform banking offers numerous benefits, it also brings with it a number of challenges and risks that financial institutions must overcome to ensure successful implementation. Below, we address the key challenges and risks associated with platform banking:

Operational complexity. Managing a diverse ecosystem of partners and services requires effective coordination and collaboration. Banks must invest in robust operational processes, relationship management, and support systems to ensure seamless communication and a consistent customer experience across the platform.

Regulatory compliance and governance. The interconnected nature of platform banking raises complex regulatory issues. Banks must comply with various financial regulations, data protection laws, and industry standards when working with external partners. Compliance in multiple jurisdictions can be challenging and requires continuous monitoring and adherence to changing regulatory requirements.

Integration issues. Integrating different systems, APIs, and services from different partners can be a technical challenge. Banks need to ensure seamless interoperability to provide a smooth experience for their customers. Compatibility issues, different data formats, and API discrepancies can arise and must be resolved to enable efficient collaboration.

While platform banking offers new opportunities for financial institutions and customers, overcoming these challenges and mitigating risks is essential for a successful and sustainable implementation. Through proactive risk management, collaboration with trusted partners, and a strong commitment to data security and compliance, banks can realize the full potential of banking platform as a service while protecting the trust and loyalty of their customers.

Future outlook of banking as a platform

The future outlook for banking as a platform is nothing short of revolutionary, with the potential for “banking platform as a service” (BPaaS) taking center stage. BPaaS will enable financial institutions to transform into agile and modular platforms that offer a wide range of services via open APIs. This seamless integration will foster collaboration with fintech startups and other industry players, leading to a rich ecosystem of interconnected financial solutions.

In addition, new and emerging technologies such as blockchain, artificial intelligence, and decentralized finance (DeFi) will play a critical role in shaping the future of the bank as a platform. These innovations will enable faster, more secure, and highly personalized financial experiences for customers.

Predictions for the evolution of platform banking over the next decade point to increased financial inclusion, a rise in sustainable financial offerings, and a shift toward customer-centric and user-friendly interfaces. As the regulatory framework adapts to the growing importance of banking as a platform, consumers can look forward to a future where financial services are connected, accessible, and tailored to their individual needs.

Accelerate innovation with SDK.finance platform banking system

SDK.finance neobank Platform serves as a powerful system for building your own banking solutions. With over 400 APIs and a modular architecture, our software Platform enables seamless integration of a wide range of banking services, giving you control over creating the ultimate banking experience for your customers.

By leveraging our pre-built core and rich APIs, you can save valuable development resources and focus on delivering best-in-class banking solutions to your customers. The FinTech Platform is loaded with essential features that enable you to create an exceptional banking experience:

- P2P money transfers

Enable quick and hassle-free money transfers between your customers, fostering seamless interactions.

- Multi-currency accounts

Offer your clients the flexibility to hold funds in multiple currencies, empowering them to manage their finances on a global scale.

- Popular payments

Integrate local vendors to facilitate utility bill payments, internet transactions, cell phone top-ups, and other popular services, providing added convenience to your customers.

- Currency exchange

Empower your clients to perform currency exchange transactions effortlessly, making it simple to operate in different currencies.

- Expense visualization

Categorize your users’ spending and present it through charts and diagrams, providing them with valuable insights into their financial habits.

- Roles and permissions management

Manage back-office access efficiently by adjusting role permissions or creating new ones to ensure secure and organized operations.

Conclusion

Platform banking is revolutionizing the financial services landscape and unleashing the power of connected financial services like never before. This innovative approach is transforming traditional banks into dynamic ecosystems where customers can seamlessly access a wide range of financial products and services.

Discover the SDK.finance neobank system to build your own banking product and turn the first years of development into the first years of growth of your customer base and revenue.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Automotive / EVs, Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- BlockOffsets. Modernizing Environmental Offset Ownership. Access Here.

- Source: https://sdk.finance/platform-banking-revolutionizing-financial-services-for-the-digital-age/