This report was written by IOSG Ventures and published exclusively on The Defiant

Acknowledgments: Special thanks to Xinshu, Lucas and Evgeny for providing valuable feedback and Darko Bosnjak for the help with data analysis!

TLDR:

- The article discusses the state of the DEX derivatives market in the post-FTX era.

- Most DEXs have struggled to attract organic growth as a large chunk of trading volume has been generated by bots and traders who exploit token economics or liquidity providers.

- GMX emerged as the largest positive surprise in the vertical. Its zero-price impact design makes it an attractive venue for whale traders.

- GMX’s product is still far from perfect, with limitations including constrained asset selection, liquidity scaling issues, a lack of adequate protocol-level risk management, a large dependency on centralized inputs, and sub-optimal UX.

- Nevertheless, some of these shortcomings might have been intentional trade-offs that helped GMX find the product-market fit and become the derivatives DEX with the most organic demand.

- Still, the market has proven that to win the crypto derivatives market share, DEXs would have to beat CEXs at their own game.

Crypto derivatives volumes have been outpacing the spot market, and the trend shows no signs of slowing down. In 2022, the top 10 derivatives centralized exchanges (CEXs) saw a daily average volume of roughly $95 billion, while the top 10 spot CEXs accounted for around $31 billion. As the industry continues to mature, we can expect the ratio of derivatives to spot volume to reach levels similar to those of traditional asset classes.

However, when we turn our attention to decentralized exchanges (DEXs), the story is a bit different. Derivatives volumes were only 56% of the spot market volumes, indicating a relative immaturity in the derivatives DEXs. This is especially apparent when we compare the DEX to CEX ratio within the specific vertical: derivatives DEXs account for a mere 1.5% of CEX volume, while the share is closer to 8% in the spot market.

| 2022 | Average Daily Volume $B | 2022 | Ratio |

| DEX spot | 2.46 | DEX spot/CEX spot | 0.077 |

| CEX spot | 31.65 | DEX der/CEX der | 0.0146 |

| DEX der | 1.40 | DEX der/DEX spot | 0.569 |

| CEX der | 95.93 | CEX der/CEX spot | 3.030 |

It’s important to note that just because derivatives generate much larger notional volume in traditional finance and centralized crypto exchanges, it does not necessarily mean we will see the same trend among decentralized players. In fact, there is only one crypto derivatives market, and it’s possible that it will continue to outgrow the crypto spot market without any contribution from DEXs.

If there was ever a moment that could serve as a strong catalyst for the growth of derivatives exchanges, it was surely the bankruptcy filing of FTX in 2022 after a series of controversial events. This unprecedented shock served as a stark reminder not to trust centralized players. But the question remains: have we truly learned the lessons this time?

Despite the unprecedented shock of FTX’s bankruptcy, recent data indicates that we may not have fully learned our lesson, or alternatively, that existing DEX solutions may not be equipped to meet the demand.

The contribution of decentralized derivatives and spot exchanges to the total crypto exchange volume has even decreased, with these platforms accounting for only around 1.3% and 6% of CEX volume, respectively. This serves as a sobering reminder that while the industry has made progress, there is still much work to be done to build a truly decentralized and trustworthy system.

| Past 30 Days | Average Daily Volume $B | Past 30 Days | Ratio |

| DEX spot | 1.6146 | DEX spot/CEX spot | 0.058 |

| CEX spot | 27.8356 | DEX der/CEX der | 0.0134 |

| DEX der | 1.1218 | DEX der/DEX spot | 0.694 |

| CEX der | 83.5994 | CEX der/CEX spot | 3.003 |

Taking a closer look at the market performance of leading players like GMX and dYdX, there doesn’t seem to be a significant increase in enthusiasm for the future of these projects. Their respective tokens are still priced at similar to lower multiples (FDV/Annualized Revenue) to those of the pre-FTX crash period, and the recent increase in multiples is reflective of the general market increase, suggesting a lack of confidence in their ability to outperform the markets by exponentially growing their volumes.

GMX FDV/Protocol Revenue (Annualized) vs Market Proxy

GMX FDV/Protocol Revenue (Annualized) vs Market Proxy

***Market proxy is taking into account protocols with revenue-generating capabilities and taking the mean of their respective FDV/Revenue ratios. It includes the following projects: Lido, AAVE, Maker, Pancake Swap, Compound, Balancer and Sushiswap

dYdX FDV/Protocol Revenue (Annualized) vs Market Proxy

So, can DEXs really take over the crypto trading game? We’ve got some important considerations to keep in mind, including the key ways that DEXs stand out from their centralized counterparts. But beyond that, we also need to delve into the practical effects of differentiation points and take a look at the various events that could either bolster or undermine their importance.

For example, if regulators were to clamp down on centralized exchanges, this could create more short-term demand for DEXs as users seek alternative trading options.

On the other hand, if the market experiences a prolonged period of stability, users may be less concerned about the potential risks associated with centralized exchanges and may opt for the convenience and efficiency they offer.

Dozens of DEXs have attempted to gain a foothold in the crypto derivatives market over the past two years, but most have struggled to attract organic growth as a large chunk of trading volume has been generated by bots and traders who exploit token economics or liquidity providers.

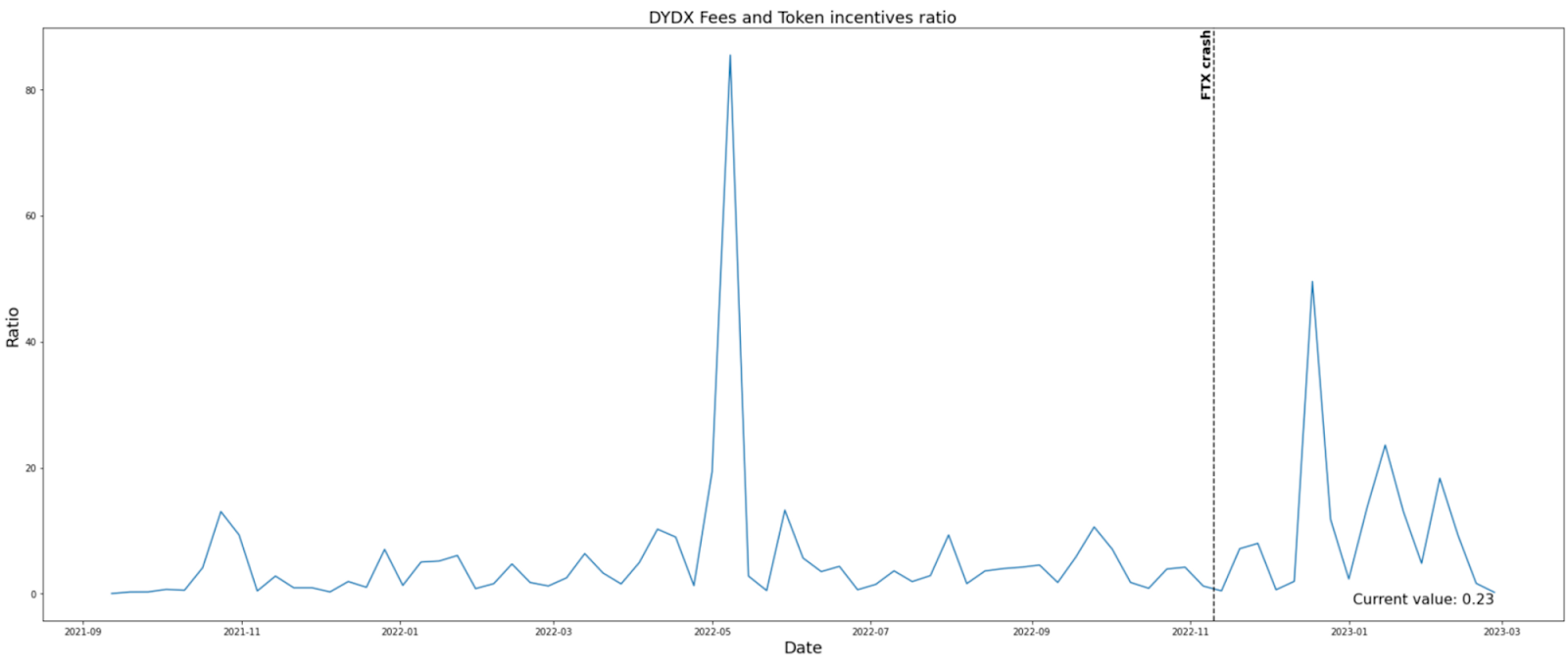

For instance, according to TokenTerminal, dYdX and Synthetix are among the top 5 dApps with the largest discrepancy between paid incentives and earned fees. Specifically, dYdX and Synthetix have a negative balance of $750 million and $650 million, respectively, indicating that they have paid more incentives than they have earned in fees.

While Synthetix has chosen to use its rewards to incentivize the supply side, i.e., the stakers who form the backbone of the network, dYdX has opted for direct incentives to trading activity via its trade mining program. Such incentives can lead to impracticality in determining the true organic activity.

For instance, some incentives indirectly incentivize trading activity as projects could inflate naïve liquidity via token mining rewards i.e. compensate LPs for the adversarial trading volume being generated at their expense.

In cases where incentives are explicitly targeted at trading activity, like with dYdX, it remains difficult to determine the extent to which the trading volume would exist without such rewards.

Is the token price increasing due to the rising exchange trading volume i.e. better fundamentals or vice versa?

Essentially, trade mining has the potential to create the fly-wheel effect, where:

- Users start mining tokens pre-token launch (could do so with delta-neutral strategies);

- Tokens get priced by the market relative to the activity on the platform, thus FOMO in the first step directly reflects on the token FDV

- High token price incentivizes even more volume generation

As a result, dYdX has been generating billions of dollars in volume daily. However, to what extent is this sustainable activity vs purely trade mining? Eventually, dYdX will run out of gas to fuel trading activity and its success would depend solely on the organic demand.

GMX: The Whales’ Darling

GMX is a decentralized cryptocurrency derivative & spot exchange that operates on Arbitrum and Avalanche. The platform allows users to trade cryptocurrencies in a peer-to-pool manner without the need for intermediaries. GMX offers a variety of advanced trading features, including limit orders, stop-loss orders, and margin trading with up to 50x leverage.

By design, GMX is built for large traders. This is due to its zero-price impact trading. It achieves zero price impact trading by utilizing a liquidity pool model (GLP) and somewhat centralized oracle price feed. It allows traders to ‘rent’ all of the liquidity from the pool at the current market prices in exchange for a 10 basis point trading fee and hourly borrowing cost.

Using $100k trading volume daily as a threshold for defining whale traders, we observe that roughly less than 10% of GMX traders could be classified as whales, yet this group of traders consistently generates more than 90% of the trading volume on the platform. This is consistent with the success stories of the majority of Tier 1 DeFi protocols, where time and time again, finding PMF requires trade-offs that favor whales.

IOSG Report: A New Financial System Will Be Built on Rollups

A Deep Dive Into What Comes Next for DeFi

How organic is the activity on GMX?

GMX has also been experimenting with innovative ways of utilizing tokens to bootstrap activity. However, its incentives are not focused on creating a false sense of traction due to the following:

a) GMX doesn’t have direct incentives for traders, such as the trade mining initiative

b) it is mostly focused on growing its TVL, but at the same implementing design choices that protect its LPs from adversarial volume i.e. it is not paying LPs to sit in the pool and tolerate arbitrage volume

Hence, most of the GMX volume is, indeed, organic. The only exception could be the possibility of some traders speculating on the potential Arbitrum airdrop to the users of ecosystem dApps.

On the importance of GLP

In comparison with typical perpetual swap contracts, GMX derivatives have a stricter ceiling as the open interest is limited by the depth of the liquidity pool to ensure the solvency of the protocol. Thus, scaling the liquidity pool has been the priority of GMX, and these objectives have been reflected in GMX token economics.

The liquidity of ETH and BTC has been the most critical for GMX as traders are mostly interested in renting out exposure to these assets, which is illustrated by the historically largest borrowing fees for these assets.

Can GLP maintain sufficient TVL levels post-liquidity mining?

Even when we ignore token mining rewards, GLP holders were able to harvest double-digit APY, which in recent periods fluctuates between 15% and 30%.

GLP Rolling APY

Critics may argue that the yield offered by GLP is not commensurate with the significant directional risk exposure that GLP holders face. However, this criticism overlooks the fact that GLP holders are not necessarily passive market makers.

While GLP may not have built-in risk management techniques, individual GLP holders have the ability to implement active hedging strategies. It is reasonable to assume that many GLP holders are doing just that:

- hedge GLP basket of assets e.g. in case LP is not comfortable with the exposure to the volatility of certain tokens in the pool.

- hedge skewed market demand

Since hedging needs are typically met off-chain, it’s difficult to gauge the exact profit and loss of individual GLP holders. But, taking into account the yield and assuming reasonable hedging costs, it’s plausible that sophisticated market players can earn high single-digit to low double-digit APY (without factoring in token rewards) even after completely hedging their exposure.

Challenges

At the moment, GLP is targeting a 50:50 ratio of volatile and stable assets, however, considering that stablecoins are largely underutilized there might be room to explore different target weights. Alternatively, GMX should find a way to increase the utilization of stablecoin assets.

Namely, one challenge facing GMX is the fact that the liquidity pool i.e. GLP is the counterparty to each trade, which means that borrowing fees are always paid to the pool regardless of the demand skew. This leaves room for imbalances and larger directional risk for GLP holders.

In contrast, in regular perpetual swaps, if the market is dominantly bullish, it implies a larger cost of maintaining long positions but also the ability to earn funding payments by taking the other side of the trade. As such, assuming the market is efficient, no rational trader would pay for a short position on GMX if they could earn for having a short position on other venues.

Similarly, when the overall market is bearish, there would be a lack of incentives to open long positions on GMX. However, since markets tend to take more leverage in bullish sentiments, this is less of a concern.

The disbalance in open interest is not the only pain point of GMX exchange. Other issues include the aforementioned liquidity scaling issues, a restrictive trading universe, and a lack of adequate risk management at the protocol level.

Furthermore, the platform’s trade-offs, such as sacrificing decentralization principles (e.g. centralized oracles) and introducing friction in the user experience (e.g. delayed trade execution), are not to be overlooked.

Finally, due to its inability to provide price discovery, GMX is doomed to always be a ‘secondary’ exchange.

Nevertheless, some of these shortcomings might have been intentional trade-offs that helped GMX find the product-market fit and become the derivatives DEX with the most organic demand.

Conclusion

“First to market seldom matters. Rather, first to product/market fit is almost always the long-term winner.”

But winning over users from centralized exchanges is no easy feat. The market has shown that being non-custodial is not enough.

Instead, DEXs will have to beat CEXs at their own game by offering an equally good user experience that includes factors such as onboarding ease, trading costs, latency, price impact, asset offerings, advanced trading features, availability, reliability, and even recovery of lost funds.

Unfortunately, nowadays on the spectrum between “don’t be evil” and “can’t be evil” exchanges, the optimal user experience requires exchanges to build closer to the left side of the spectrum.

However, as the technology matures, it would become possible to move towards the right-hand side without sacrificing UX. Thus, having a long-term perspective in mind, DEXs are positioned on the winning side of the spectrum.

But, CEXs are not without recourse in this developing landscape. We shall expect them to gradually improve their standards and try to defend their market position by adopting cryptographic solutions, firstly offering a hybrid model that lessens custody & transparency-related concerns, and ultimately, once primitive evolve enough not to require UX sacrifices, even fully becoming decentralized.

Momir Amidzic is a senior associate at IOSG Ventures.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: https://thedefiant.io/iosg-research-derivative-dexs/