In this analysis, we’ll delve into the contrasts between traditional and digital banking, highlighting user experiences, growth patterns, and the innovations that set digital banks apart. Additionally, we’ll explore whether the rise of digital banks truly poses a significant threat to the longevity of traditional banking institutions.

What are Digital Banks?

In the vast realm of finance, digital banks have emerged as a modern solution to traditional banking’s limitations. Operating solely online or through mobile apps, these banks lack the physical branches that many are accustomed to. Instead, they harness the power of technology to offer a range of financial services, from standard current accounts to intricate financial tools, all at the fingertips of their users. Examples of prominent digital-only banks in the UK include Monzo, Starling Bank, Revolut, and Chase. These banks have rapidly gained popularity, providing competitive alternatives to their traditional counterparts. The primary distinctions between digital and traditional banks lie not just in their physical presence (or lack thereof) but also in their operational approaches:

- Cost Efficiency: Without the overheads of maintaining brick-and-mortar branches and large staff numbers, digital banks often pass on the savings to customers through lower fees and better interest rates.

- Speed & Accessibility: The online nature of digital banks allows for 24/7 access, real-time updates, and quicker transaction processes.

- Innovative Features: Many digital banks lead in innovation, offering tools for budgeting, savings, and even investment, often integrated directly into their platforms.

- Regulatory Framework: Both digital and traditional banks are subject to financial regulations, but digital banks face unique challenges. For instance, the Financial Conduct Authority (FCA) in the UK has tailored specific regulations for digital banks, focusing on aspects like cybersecurity, data protection, and online transaction handling. These regulations are often more stringent or different in nature compared to those for traditional banks, reflecting the unique risks and operational models of digital banking.

However, it’s essential to note that the heart of banking—safekeeping funds, facilitating transactions, and providing financial services—remains consistent across both digital and traditional platforms.

Popularity & Growth of Digital Banks

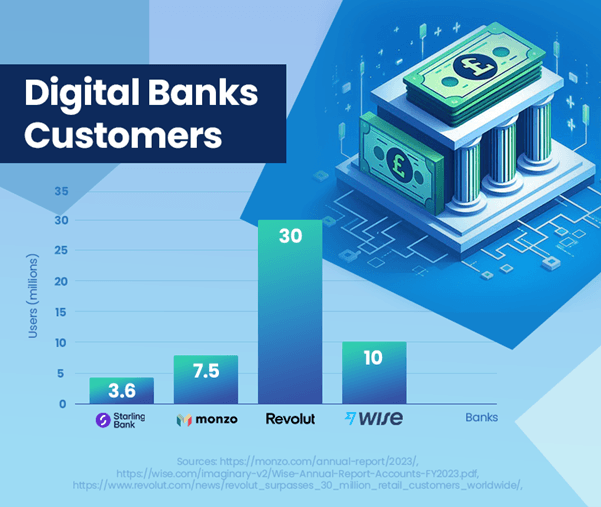

The rise of digital banks in the UK signifies a notable shift in consumer banking preferences. These banks have shown impressive growth in user numbers and market presence. Monzo has reported 7.5 million users[1], and Starling Bank’s UK user base reached 3.6 million[2], showcasing their increasing popularity. In contrast, HSBC, a major traditional bank, boasts 39 million customers[3], highlighting the scale difference between established and emerging banking models.

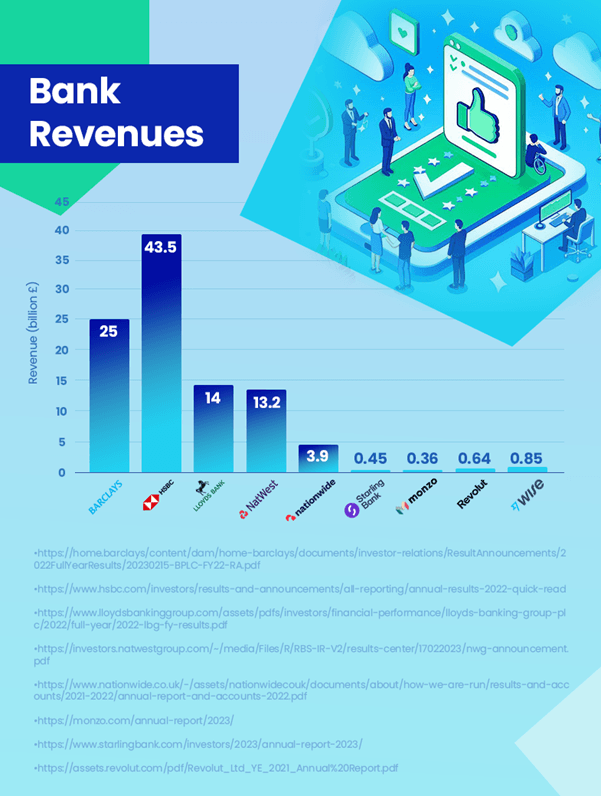

When it comes to revenue, traditional banks still lead by a significant margin. HSBC, for instance, recorded a revenue of £43.5 billion[4]. In comparison, the most profitable digital bank, Wise, generated £0.85 billion[5] in revenue. Following behind are Revolut with £0.64 billion[6] and Starling with £0.45 billion[2]. It’s important to note that Revolut’s figure is from 2021, and its revenue could be higher now. Although digital banks are growing, they are still far behind traditional banks in terms of revenue generation.

Despite the impressive growth trajectory of digital banks, their current market share does not pose a significant threat to the dominance of traditional banks. A key consideration is that many consumers may not be using digital banks as their primary accounts. It’s common for people to maintain accounts with larger traditional banks while also exploring the services offered by digital banks. This dual-banking approach suggests that the impact of digital banks on traditional institutions is more complementary than outright competitive at this stage.

However, the future trajectory for digital banks is positive, with expectations of continued user growth and market penetration. This trend could prompt traditional banks to further innovate and adapt, especially in the realms of digital user experience and financial technology.

This data highlights that while digital banks are making significant inroads, they currently serve more as a complement to the traditional banking model rather than a direct replacement.

How do Revenues Compare for Digital and Traditional Banks?

The comparison of revenues between digital and traditional banks provides valuable insights into the current banking landscape. Traditional banks, such as HSBC, have maintained their lead in revenue generation, with HSBC reporting £43.5 billion in 2023. Their extensive range of services, larger customer base, and international presence significantly contribute to this.

Digital banks, while growing rapidly in user base, still report modest revenues in comparison. Wise, the most profitable digital bank, reported £0.85 billion in revenue, indicating that digital banks are steadily carving out their market share.

The growth trajectory of digital banks focuses on user-friendly platforms and innovative services, positioning them well for future growth. Their lower operational costs and technological advancements are key drivers in this growth trajectory.

In response to the rise of digital banks, traditional banks are evolving to expand their digital offerings. A notable example is JPMorgan Chase’s launch of Chase in the UK in 2021, a digital bank aimed at capturing the growing market for digital-first banking solutions. This initiative demonstrates how traditional banks are adapting to stay competitive and meet changing consumer preferences in the digital era.

Overall, while traditional banks currently have a significant lead in revenue, the growing presence and influence of digital banks in the market are driving industry-wide changes. The future banking landscape may see a narrowing revenue gap as digital banks continue to expand and traditional banks adapt.

User Satisfaction: Digital vs Traditional Banks

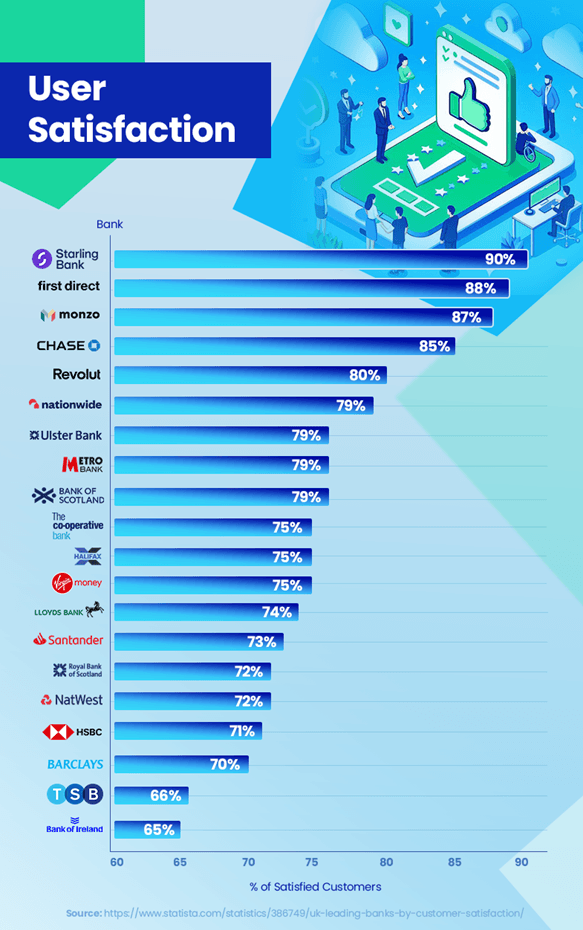

In the competitive landscape of banking, customer satisfaction is a key differentiator. Recent trends and data reveal interesting insights into how digital and traditional banks fare in this regard. Digital banks have been garnering high customer satisfaction ratings. Starling Bank leads with an impressive 90% satisfaction rate, followed closely by Monzo Bank at 87%, and Chase at 85%[7]. These high scores reflect their focus on user experience, innovative features like real-time transaction notifications, and personalized budgeting tools that resonate well with their customer base.

In contrast, traditional banks have faced challenges in keeping pace with these satisfaction levels. For example, HSBC and Barclays Bank have satisfaction rates of 71% and 70% respectively[7]. While they maintain a strong customer base, issues such as longer wait times for customer service and less agile responses to technological advancements have been points of contention for some customers.

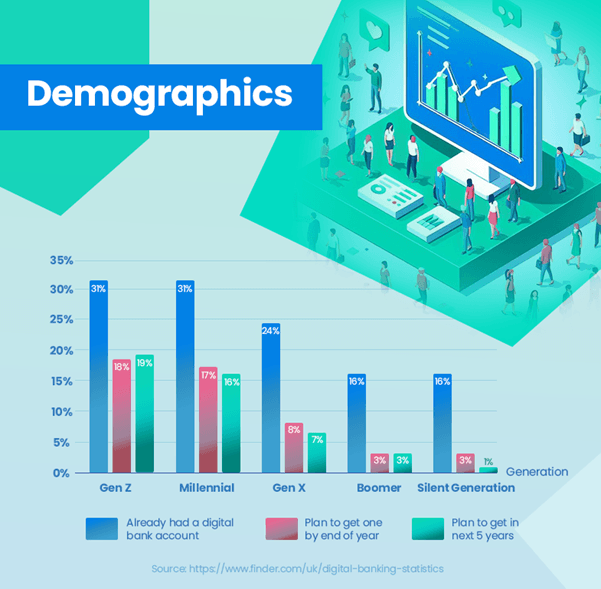

The adoption of digital banking shows a distinct trend across different age groups. A significant proportion of younger generations have already embraced digital banks – 31% of Gen Z and Millennials already have digital bank accounts, reflecting their preference for technology-driven banking solutions. This is in stark contrast to older generations, where adoption rates are notably lower – only 24% for Gen X, 16% for Boomers, and 13% for the Silent Generation[8]. This data clearly illustrates the stronger inclination towards digital banking among younger users, while older generations still lean towards traditional banks.

However, traditional banks are not static in this scenario. Many are investing heavily in digital transformation to enhance online banking experiences, aiming to bridge the satisfaction gap.

Trust and security remain paramount in banking. Digital banks have to continuously prove their reliability and safety, while traditional banks need to innovate without compromising the trust they have built over decades.

Overall, while digital banks currently lead in customer satisfaction, the evolving efforts of traditional banks suggest a competitive landscape focused on improving customer experiences across the board.

Possible Explanations for Higher Satisfaction

Digital banks achieving higher customer satisfaction rates compared to traditional banks can be attributed to several factors. Digital banks focus intensely on customer experience. Their platforms, often driven by innovative technology, are designed to be user-friendly and intuitive. This focus on the customer journey translates into higher satisfaction rates.

Digital banks are typically more agile and quicker to adopt new technologies. Features like real-time notifications, budgeting tools, and easy account management directly on mobile apps cater to the needs of a digitally savvy customer base.

Personalization is another strong suit of digital banks. They leverage data analytics to understand customer needs and preferences, allowing them to tailor their services more effectively. Being digital-first, these banks can rapidly iterate and improve their services based on customer feedback. This responsiveness ensures that they are continually evolving to meet changing customer expectations.

The convenience of managing finances from anywhere at any time is a significant draw. Digital banks eliminate the need for physical branch visits, aligning with the lifestyle of modern consumers who prefer online transactions.

These factors collectively contribute to the higher satisfaction rates among digital bank customers. As digital banks continue to innovate and tailor their services, they are likely to maintain or even increase this satisfaction advantage over traditional banks.

What Features of Digital Banks Attract Users?

The growing popularity of digital banks can be largely attributed to their distinctive features, which align well with modern consumer needs and preferences. The user-friendly interface and seamless banking experience offered by digital banks, often through mobile apps, is a significant draw, especially for tech-savvy generations who value efficiency and simplicity in their transactions.

Built-in budgeting tools in platforms like Monzo and Starling Bank provide users with the ability to track spending, set financial goals, and manage their finances more effectively. This resonates particularly with younger users who are keen on using technology to enhance their financial literacy and control.

The effortless signup process is another highlight of digital banks. Users can set up an account within minutes, without the need to visit a branch, which is a stark contrast to the often lengthy procedures of traditional banks.

Digital banks also fill the gap in areas where traditional bank branches have closed. They offer essential banking services, ensuring that people in these areas are not left financially underserved.

Banks like Starling allow for easy international payments and currency exchanges, often with lower fees compared to traditional banks. This is particularly beneficial for those who travel frequently or engage in international transactions.

Innovative features such as the ability to block gambling transactions, creating virtual cards, and offering real-time notifications for transactions provide a level of control and customization that traditional banks often lack.

These features collectively make digital banks highly appealing, especially to those who seek a banking experience that’s aligned with the digital age. As a result, digital banks are not just a choice but a preference for an increasing number of consumers.

Conclusion

The banking sector is witnessing a pivotal shift with the emergence of digital banks, challenging traditional banking institutions. This evolution is driven by changing consumer preferences, technological advancements, and the innovative approaches of digital banks.

While traditional banks continue to lead in terms of revenue and customer base, digital banks are rapidly gaining ground, especially among younger generations who favour ease of use, innovation, and digital integration in their banking experience.

The future of banking appears to be a blend of both worlds. Traditional banks are increasingly adopting digital strategies to stay competitive, while digital banks strive to expand their services and customer trust. This balance suggests a more customer-centric banking environment, where choice and convenience are paramount.

Both types of banks will need to continue adapting to consumer needs and technological trends. For traditional banks, this might mean further digital transformation. For digital banks, the focus may be on expanding their services and enhancing security and trustworthiness.

As the competition intensifies, it will likely spur further innovation and improvement across the sector, benefiting consumers with better services, more choices, and enhanced banking experiences.

In conclusion, the banking landscape is undergoing a significant transformation. The rise of digital banks marks a new era in finance, one that promises to reshape how banking services are delivered and experienced by customers.

References

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.bestcasinosites.net/blog/digital-banks-vs-traditional-banks.php