Receive free Non-fungible tokens updates

We’ll send you a myFT Daily Digest email rounding up the latest Non-fungible tokens news every morning.

Inbox:

The Securities and Exchange Commission today charged Stoner Cats 2 LLC (SC2) with conducting an unregistered offering of crypto asset securities in the form of purported non-fungible tokens (NFTs) that raised approximately $8 million from investors to finance an animated web series called Stoner Cats.

Deep breaths.

Stoner Cats is an “NFT adult animated short series”, which means basically nothing in theory but in practice looks like this:

Listen up mfs (my friends): episode 6 comes out December 23rd!! 👵🏼❤️🤶🏼 pic.twitter.com/hgQrvcaE4i

— Stoner Cats (@stonercatstv) December 15, 2022

[please if anyone watches this and recognises the sound at 0:15 when the packet hits the fire let us know it’s driven FTAV insane . . . is it from a video game? arrgghhh.]

A 2021 article by Forbes asked . . .

. . . but didn’t really make any attempt to answer that presumably easy question. The SEC frames it thusly:

Actor Mila Kunis (whose production studio Orchard Farm Productions produced this production) and her himbo husband Ashton Kutcher, the article says, called Stoner Cats a “new model for watching a cartoon TV show about a group of weed smoking felines”. We don’t know what the old model was.

Anyway, Kunis and Kutcher voiced some cats, while Vitalik Buterin (who co-founded Ethereum) also played a character, blah blah blah the passage of time. Now:

According to the SEC order, on July 27, 2021, SC2 offered and sold to investors more than 10,000 NFTs for approximately $800 each, selling out in 35 minutes. The order finds that both before and after Stoner Cats NFTs were sold to the public, SC2’s marketing campaign highlighted specific benefits of owning them, including the option for owners to resell their NFTs on the secondary market.

In addition, the order finds that, as part of the marketing campaign, the SC2 team emphasised its expertise as Hollywood producers, its knowledge of crypto projects, and the well-known actors involved in the web series, leading investors to expect profits because a successful web series could cause the resale value of the Stoner Cats NFTs in the secondary market to rise.

Further, the order finds that SC2 configured the Stoner Cats NFTs to provide SC2 a 2.5 per cent royalty for each secondary market transaction in the NFTs and it encouraged individuals to buy and sell the NFTs, leading purchasers to spend more than $20 million in at least 10,000 transactions. According to the SEC’s order, SC2 violated the Securities Act of 1933 by offering and selling these crypto asset securities to the public in an unregistered offering that was not exempt from registration.

Carolyn Welshhans, associate director of the SEC’s home office, said:

Registration of securities, including crypto asset securities, protects investors by providing them with disclosures so they can make informed investing decisions. Stoner Cats wanted all the benefits of offering and selling a security to the public but ignored the legal responsibilities that come with doing so.

The Stoner Cats did not land on their feet, and appear to have rolled over:

Without admitting or denying the SEC’s findings, SC2 agreed to a cease-and-desist order and to pay a civil penalty of $1 million.

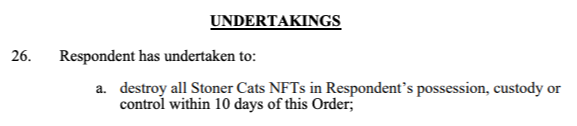

You probably have to laugh, else you’d cry. But Alphaville, which often does both, was most interested by this section from the SEC’s order:

Wha . . . ? Besides the fact that the company claimed the 10,000 NFTs sold out within minutes — what is this supposed to mean? (Nb the SEC used the “destroy” word in another order, against Impact Theory, last month.)

An NFT, as has been pointed out ad nauseam, boils down to a unique identifier stored on a blockchain that points to a typically digital asset (ie a shitty JPEG), its owner, and the associated smart contract. The asset element is only referenced by a link, which could break and is therefore one of many, many reasons NFTs are dumb.

In this context, the only bit of the NFT that is intrinsically the NFT is the identifier itself.

But this element is on the blockchain, which means it can never be destroyed! At the risk of sounding, well, stoned, how does one destroy an un-destroyable digital commodity?

The common practice in this situation seems to be to transfer the NFT to a wallet that nobody controls, and that acts like a huge communal trash can — a process known as “burning” the NFT. So it’s still there, but nobody can get it.

Will the SEC be happy with this concept of destruction? We’ve asked regulators the question, and will update if we get a response.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.ft.com/content/caf40a55-8673-40d4-a10e-46778e207677