Geopolitical turbulence and the fragile and volatile nature of

the critical raw-material supply chain could curtail planned

expansion in battery production—slowing mainstream

electric-vehicle (EV) adoption and the transition to an electrified

future.

Soaring prices of critical battery metals, as observed in the

following chart from S&P Global Commodity Insights, are

threatening supplier and OEM profit margins. This situation has

quickly translated into increased component and vehicle prices,

according to new analysis from S&P Global Mobility Auto Supply

Chain & Technology Group.

Trade friction and ESG concerns are also affecting the

development of the raw materials supply chain between markets.

These collective developments add to the challenges of the electric

vehicle transition.

Achieving its volume goals will require a steep growth curve for

a burgeoning industry. For OEMs to hit their BEV and hybrid sales

aspirations, S&P Global Mobility forecasts market demand of

about 3.4 Terawatt hours (TWh) of lithium-ion batteries, annually,

by 2030. This figure excludes the medium- and heavy-duty, and

micro-mobility spaces, as well as consumer electronics and

burgeoning demand for stationary energy storage. The 2021 output

for the auto industry: 0.29 TWh.

Elements such as lithium, nickel, and cobalt do not just

magically appear and transform into EV batteries and other

components. The development chain is lengthy and complex, from

their difficulty to extract to their complicated refining. The

intermediate steps between excavation and final assembly are a

particular choke point in terms of expertise and market presence.

Currently, China is the clear leader in materials refining, as well

as the packaging and assembly of battery cells. At issue is which

other nations will step up to facilitate this industry

transformation.

In terms of accessing battery raw materials, the equation boils

down to: Who needs what, where will it come from, who will supply

it, and who is best placed to benefit from this increased

dependency on a handful of critical elements?

The latest S&P Global Mobility research evaluates the

battery raw material supply chain from extraction to vehicle,

identifying:

- A number of unfamiliar companies will play a major role in the

processing and development of battery-electric vehicle (BEV)

technology that will underpin the light passenger vehicles of the

coming decade and beyond; - Potential trade friction could represent difficulties for major

auto companies in extricating themselves from an established,

nimble, and cost-effective supply of processed materials coming

from or via mainland China; - Some OEMs are seeking the value and reassurance of “locked in”

supply chain relationships straddling mine to vehicle, lessening

the reliance on volatile spot markets and/or a need to work with

less established industry partners.

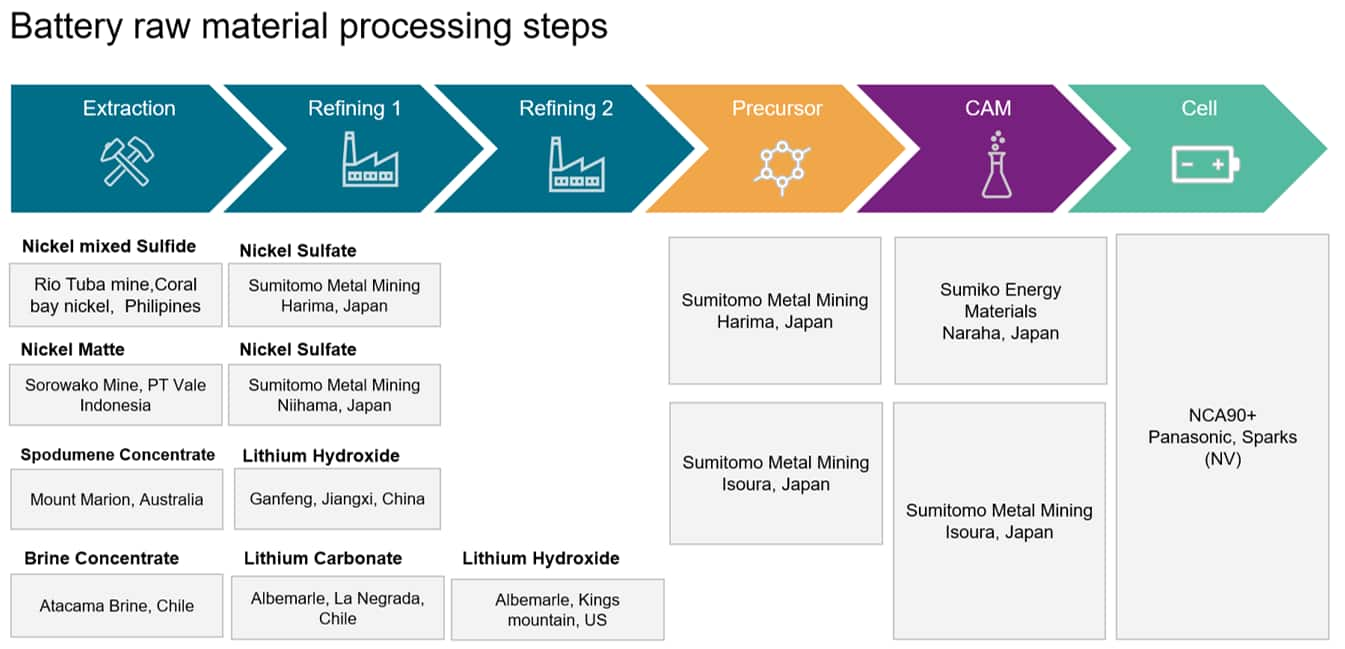

The process flow below identifies a well-understood and

well-documented supply chain to provide the required nickel and

lithium for Tesla’s NCA-based cylindrical cells produced in its “Gigafactory” near Sparks, Nevada, US.

Now extrapolate that across the entire auto industry—and

expand EV market share to encompass the bullish projections made

for 2030 and beyond.

The greatest quantity of nickel required by any given vehicle

brand for 2030 production is forecast to be Tesla—deemed to be

some 139,000 metric tons (mT). However, in assessing the existing

structure of their broader manufacturing bases, we expect each of

Volkswagen, General Motors, and Stellantis to surpass this

requisition amount. Developing modular battery packs that can be

configured to fit multiple vehicle segments and can accommodate a

variety of battery chemistry choices will ensure a degree of

resiliency against raw material supply constraints and price

fluctuations.

“We have identified a total of 28 extraction sources of

battery-grade nickel over the coming 12 years to serve the light

passenger-vehicle market, located in 15 countries worldwide,” said

Dr Richard Kim, Associate Director with S&P Global Mobility’s

Supply Chain & technology team. “However, the supply base for

the upstream material processing steps and formation of the

fundamental battery cell cathode chemistries presents a challenging

lack of geographic diversity.”

S&P Global Mobility research suggests that, while the

process of either smelting or high-pressure acid leaching (HPAL) is

typically done at the nickel extraction site, that is not the case

for the process of conversion to nickel sulphate.

Of the 16 companies that can perform this process at present, 11

are in mainland China. By 2030 we expect the number of companies to

increase to at least 24, of which 14 will likely be in mainland

China. We forecast mainland China to process 824,000 mT of nickel

sulphate annually by 2030, with Chinese mining giant GEM’s supply

of nickel sulphate to key Tesla supplier CATL expected to be the

largest supply contract by tonnage. By contrast, we forecast North

America and Europe to process just 146,000 mT.

We must also consider risk in calculating access to cobalt—a

material well understood for its limited sources of origin and

concerns regarding ethical supply. Battery-grade cobalt bound for

electrified light passenger vehicles currently originate from just

18 mines, totalling 52,000 mT – of which 29,000 mT is forecast to

be mined in the Democratic Republic of Congo (DRC) in 2022. The

United Nations has cited the DRC’s “deteriorating security

situation,” its humanitarian crisis affecting 27 million people, as

well as child-labor practices and the ongoing guerrilla campaign

being waged over the exploitation of resources and food

security.

Despite the conflicts ravaging the DRC, we still estimate that

nation’s output bound for OEMs and suppliers to increase to 37,000

mT by 2030. However, reliance on the DRC will decrease from 56% to

17% in terms of total tonnage. We expect near tenfold increases in

supply from countries such as Australia and Indonesia, while

countries such as Vietnam, Finland, and Morocco will by then weigh

in with meaningful contributions. Given the dynamics of the supply

market, even for an OEM with locked-in cobalt contracts with

miners, a portion of several automakers’ supply remains unknown at

this stage.

“Geopolitics has coupled with a desire for supply chain

dominance and independence in the battery raw material supply chain

evolution to date,” said Dr Kim. “China has established a firm head

start. The evolution of their Belt and Road initiative clearly had

one eye on the automotive industry transition to electrification,

with broad strategic and logistical investments in Africa as well

as Southeast Asia.”

S&P Global Mobility research clearly indicates that

established battery raw material supply and processing operations

under mainland Chinese ownership will continue to deliver much of

the world’s supply of lithium-ion batteries and their constituent

key elements.

However, the imposition of nationalistic policies such as the

United States’ Inflation Reduction Act (and the automotive

implications of it) look to belatedly redress some of this

imbalance by promoting the setup of domestic supply chains, in

return for lucrative subsidies to both the suppliers and the

purchasing consumers.

The battery will be the defining technological and supply chain

battleground for the industry in the next decade, and access to

their constituent raw materials will be crucial. S&P Global

Mobility will continue to assess the changing landscape of the

battery raw materials market in real time, incorporating the latest

industry developments and research.

Please contact automotive@spglobal.com

to find out more information around our insights to help you make

data-driven decisions with conviction.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

- Coinsmart. Europe’s Best Bitcoin and Crypto Exchange.Click Here

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: http://www.spglobal.com/mobility/en/research-analysis/a-reckoning-for-ev-battery-raw-materials.html