Britain is gearing up to impose a carbon tax on imported goods in a move announced by the Treasury aimed at safeguarding UK firms against being outcompeted by foreign manufacturers.

The proposed tax, also called the Carbon Border Adjustment Mechanism (CBAM) is set to take effect in 2027. It aims to ensure that imports like iron, steel, aluminum, ceramics, and cement face a similar carbon price to domestic goods. The move intends to maintain fairness in the market.

What is the UK CBAM?

Governments use a carbon price as a tool to curb emissions by imposing charges on carbon pollution. The goal is to encourage industries to reduce their greenhouse gas emissions.

Chancellor Jeremy Hunt highlighted the role of their British CBAM version, saying:

“This levy will make sure carbon-intensive products from overseas — like steel and ceramics — face a comparable carbon price to those produced in the UK so that our decarbonization efforts translate into reductions in global emissions.”

The UK government noted the new tax would help address “carbon leakage” which has become more pressing. This means avoiding emissions being displaced to other countries that have lower or no carbon pricing mechanisms in place.

The CBAM will work hand-in-hand with the UK Emissions Trading Scheme. It’s the same as how the EU’s CBAM functions in parallel with the EU’s ETS.

According to the Treasury, these plans will help level the playing field and encourage greater investment in net zero efforts.

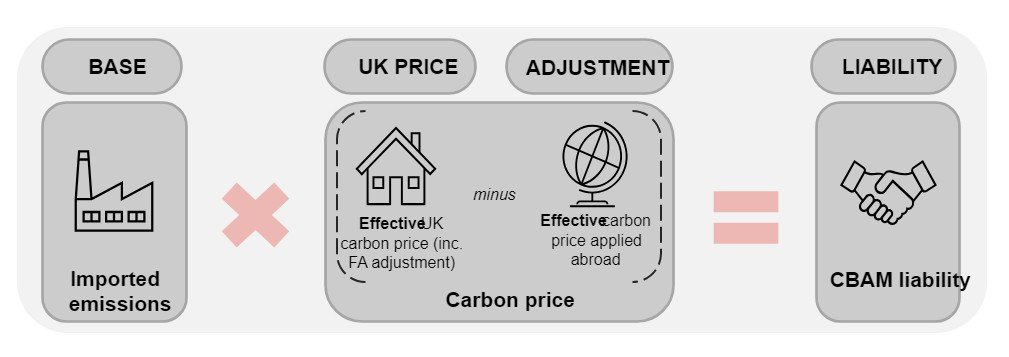

Under the proposed CBAM, charges will be determined based on the volume of carbon emissions produced during product manufacturing. The difference between the carbon price applied in the country of origin and that paid by comparable UK manufacturers will also influence these charges.

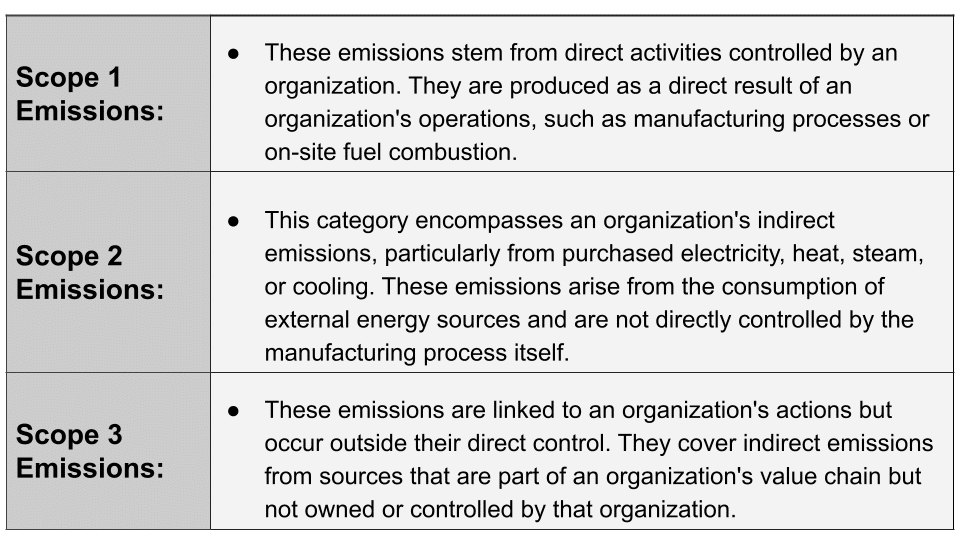

What Emissions Scope is Covered?

The importer of imported products covered by the UK CBAM will be liable for the tax based on the products’ embodied emissions. It will not include the trading of emissions certificates.

The emissions scope categories that would be under CBAM are as follows:

The UK CBAM will also extend its coverage to Scope 1, Scope 2, and specific precursor product emissions found in imported products. This extension aims to align with the coverage provided by the UK ETS.

The UK ETS is designed to regulate and put a price on GHG emissions produced by domestic industries. Operating on a cap-and-trade mechanism, this system allows the market to determine the value of emission allowances. The total carbon emissions allowed and the corresponding allowances are capped under this scheme, gradually decreasing over time.

As part of the strategy to address the risk of carbon leakage within sectors covered by the UK ETS, a segment of UK ETS allowances (UKAs) is allocated to operators in exposed sectors without charge. This allocation ensures that certain operators receive allowances for free, thereby reducing their exposure to the carbon price.

However, this measure also retains the economic motivation for these operators to invest in decarbonization initiatives. Thus, it maintains the overall emissions cap across the sectors included in the ETS.

Closing Carbon Loopholes

Following a consultation on solutions for carbon leakage, the Treasury reported that 85% of respondents identified the issue as a present or future risk to their efforts in achieving decarbonization.

There’s a growing concern that while companies in the UK work towards reducing GHGs, equivalent efforts are not mirrored abroad. This gap may result in emissions merely shifting to countries without ambitious net zero targets, providing limited global environmental benefits.

To address these concerns, implementing a suitable carbon price like CBAM is considered a significant step to mitigate carbon loopholes.

The Treasury plans to engage in further consultations in 2024 concerning the levy’s specifics. These include its design, implementation, and the comprehensive list of goods and products subject to the levy.

Moreover, it seeks input from various sectors, including power, aviation, and industry, regarding the UK Emissions Trading Scheme.

The Chairman of the Environmental Audit Committee emphasized the necessity of addressing emissions associated with imports, constituting 43% of the UK’s consumption emissions. This is to prevent undermining the UK’s decarbonization efforts.

Implementing an appropriate carbon price at the border will play a crucial role in closing carbon loopholes.

The UK’s introduction of the carbon tax marks a significant step toward aligning carbon pricing and ensuring fairness in global markets. By covering a wide scope of emissions, the CBAM intends to close carbon loopholes, encouraging industries to invest in net zero efforts and supporting the nation’s decarbonization journey.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://carboncredits.com/uk-reveals-move-for-a-carbon-border-tax-in-2027/