Tag: margin

4 Education Resources You May Have Missed This Month

Take a moment to read our roundup of content and resources to bring ideas, insight and inspiration into the week ahead – and beyond. While districts still face many challenges due to COVID, we also want to share the resilience and adaptability many districts have shown as they work to educate students in a “not so normal world.“

Fast Facts About Digital Transformation And The Pandemic

Our infographic highlights the benefits and importance of digitizing the supply chain and how users that deploy a supply chain management solution can analyze and act on the data derived from a fully connected, intelligent, and transparent supply chain. Read more about the benefits in our '5 WAYS DIGITAL TRANSFORMATION HELPS YOU MAKE INFORMED DECISIONS'

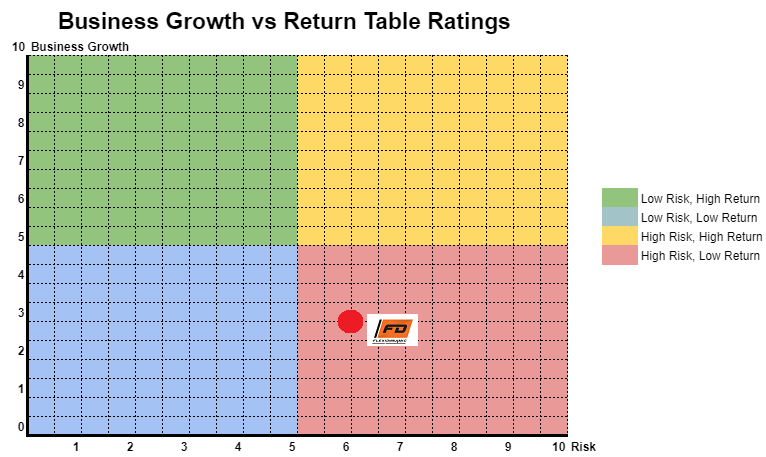

Flexidynamic Holdings Berhad

Close to apply: 16/03/2021

Listing date: 30/03/2021

Market Cap: RM56.778mil

Total Shares: 283mil shares (Public apply: 14.1 mil, Company Insider/Miti/Private Placement/other: 61.036mil)

Flexidynamic: RM31.31mil

Polydamic Group Bhd: RM11.78mil

Ripcol Industries S/B: RM17.2mil

Business

Design, engineering, installation, & commissioning of glove chlorination system.

M'sia: 86.28%

Vietnam: 4.38%

Thailand: 8.74%

Indonesia: 0.07%

Sri Lanka 0.53%

Fundamental

1.Market: Ace Market

2.Price: RM0.20 (EPS:RM0.0162)

3.P/E: PE12.35

4.ROE(Pro Forma III): 10.1%

5.ROE: 21.4%(2019), 24.8%(2018), 33%(2017)

6.Cash & fixed deposit after IPO: RM0.059 per shares

7.NA after IPO: RM0.12

8.Total debt to current asset after IPO: 0.708 (Debt: 31.832mil, Non-Current Asset: 21.998mil, Current asset: 44.976mil)

9.Dividend policy: Did not have formal dividend policy.

Past Financial Performance (Revenue, Earning Per shares)

2022: ***Remaining order book to be billed 2022 RM17.48mil

2021: ***order book to be billed Dec 2021 RM62.3mil

2020 (9mths): RM35.007 mil (EPS:0.0095)

2019: RM49.839 mil (EPS:0.0162)

2018: RM48.322 mil (EPS:0.0151)

2017: RM29.902 mil (EPS:0.0155)

Net Profit Margin

2020 (9mths): 7.62%

2019: 9.22%

2018: 9.14%

2017: 14.79%

After IPO Sharesholding

Tan Kong Leong: 41.53%

Liew Heng Wei: 18.74%

Phitchaya Arsangku: 2.21%

Directors & Key Management Remuneration for FYE2021 (from gross profit 2019)

Total director remuneration: RM1.168mil or 8.37%

key management remuneration: RM0.4mil- 0.5mil or 2.87%-3.58%

total (max): RM1.668mil or 11.95%

Use of fund

Repayment bank borrowing: 42.40% (purchase of 2 new factories 2019)

Renovation of new factories: 2.80%

Aquisition of machinery and equitment: 10.83%

Working capital: 24.03%

Listing Expenses: 19.94%

Good thing is:

1. Revenue increasing over 3 years.

2. Debt ratio not too dangerous level.

4. Major customer Hartalega, contribute to Flexidyamic revenue 2017-2020 (range 31.78%-40.91%).

1. Director fees & key managemnent remuneration already cost 11.95% from the company gross profit.

2. Net profit percentage dropping since 2017.

3. No fixed dividend policy.

4. ROE continue to fall over 3 years.

5. Industry player for top 2 & top 3 revenue RM17mil & RM11mil, showing this industry is not generate high revenue (possible less demand of the project needed).

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion)

2020 is the high demand for glove, however did not see large improvement in net margin. The company secure RM62mil order book to be billed in 2021. We should see revenue able double at 2021 due to one off high demand order book due to the pandemic. After 2021, business revenue should back to normal phase. For business growth vs risk table please refer as below chart.

Beating Your Chemical Supply Chain Challenges | Roambee

Chemical supply chains stand at the crossroads of another upgrade; on one end there are traditional methods that pose challenges and on the other you have compelling technology solutions. Discover the significant challenges that lack of real-time visibility brings and how your organization can cope with them better.

Teladan Setia Group Berhad

Close to apply: 02/03/2021

Listing date: 16/03/2021

Market Cap: RM386.543mil

Total Shares: 805.298 mil shares (Public apply: 40 mil, Company Insider/Miti/Private Placement/other: 161.595mil)

Property development

Business mainly in Melaka

Residential: 51%

Mixed development: 49%

1.Market: Ace Market

2.Price: RM0.48 (EPS:RM0.054)

3.P/E: PE8.9

4.ROE(Pro Forma III): 10.36%

5.ROE: 12.60%(2019), 16.19%(2018), 22.27%(2017)

6.Cash & fixed deposit after IPO: RM0.1153 per shares

7.NA after IPO: RM0.54

8.Total debt to current asset after IPO: 0.56 (Debt: 214.877mil, Non-Current Asset: 266.719mil, Current asset: 381.972mil)

9.Dividend policy: 20% of PAT as dividend.

2020 (9mths): RM100.028 mil (EPS:0.022)

2019: RM232.988 mil (EPS:0.054)

2018: RM259.141 mil (EPS:0.061)

2017: RM359.511 mil (EPS:0.078)

2020 (9mths):19.1%

2019: 18.6%

2018: 18.8%

2017: 17.49%

Teo Lay Ban: 41.6%

Teo Lay Lee: 11.1%

Teo Siew May: 11.1%

Total director remuneration: RM1.678 mil or 2.08%

key management remuneration: RM0.90 mil-1.05mil or 1.12%-1.30%

total (max): RM2.728mil or 3.38%

Land acquisition: 45.3%

Working capital for project development: 42.8%

Repayment of bank borrowings: 5.2%

Listing Expenses: 6.7%

1. IPO price fair with the company value, PE8.9.

2. Have profit margin of 17%-19% rannge.

3. Directors & Key Management Remuneration is not too expensive.

1. Property development industry is effected by current overall economic.

2. ROE is less than 15%

Overall is fair valuation, but current economic situation is not encouraging property market to grow. Property market will need to wait at least more than 2 year to better demand. Invest in this IPO might need more time to wait and need to continue monitoring their performance. For business growth & business risk please refer to below chart.

Empowering Fresh Produce Logistics with Real-Time Data | Roambee

Dealing with fresh produce logistics means dealing with supply chains that are more prone to risk. The risk of spoilage is an additional risk to consider beyond delay and theft. When working with fresh produce supply chains, reliable condition and location tracking data is vital to prevent the risk of spoilage that can contribute to cost in the form of replacement and reshipping — increasing the overall financial loss. Let’s explore how real-time data can help keep the fresh produce supply chain lean and reduce financial losses.

Whether “roomers or Zoomers,” Lightspeed offers “crystal clear sound”

Fourth grade special education teacher Jaimee Rothenberg says the Lightspeed classroom instructional audio system was an important tool before the COVID-19 pandemic, helping students with auditory issues who may have otherwise needed preferential seating, and helping all students hear lessons more clearly.

Mobilia Holdings Berhad

Open to apply: 03/02/2021

Close to apply: 09/02/2021

Listing date: 23/01/2021

Share Capital

Market Cap: RM92mil

Total Shares: 400 mil shares (Public apply: 20mil, Company Insider/Miti/Private Placement/other: 80mil)

Industry (Net Profit %)

Homeriz: 15.18%

Spring Art: 13.14%

Mobilia: 11.14%

Liihen: 9.51%

Business

Design & Manufacturing of home furniture.

Oversea: 73.39%

Malaysia: 26.61%

*2017-2020: 50.48%-56.48% revenue come from 5 major customer.

Fundamental

1.Market: Ace Market

2.Price: RM0.23 (EPS:0.02)

3.P/E: PE11.50

4.ROE(Pro Forma III): 17.29%

5.ROE: 35.71%(2019), 27.55%(2018), 31.45%(2017)

6.Cash & fixed deposit after IPO: RM0.0406 per shares

7.NA after IPO: RM0.10

8.Total debt to current asset after IPO: 1.176 (Debt: 39.385mil, Non-Current Asset: 45.954mil, Current asset: 33.447mil)

9.Dividend policy: No fixed dividend policy.

Past Financial Performance (Revenue, EPS)

2020 (8mths): RM44.729 mil (EPS:0.0136)

2019: RM75.589 mil (EPS:0.0248)

2018: RM66.504 mil (EPS:0.0184 )

2017: RM55.730 mil (EPS:0.0184)

Net Profit Margin

2020 (8mths): 10.31%

2019: 11.14%

2018: 9.39%

2017: 11.24%

After IPO Sharesholding

Quek Wee Seng: 74.56% (Exelient & Firstchrome)

Quek Wee Seong: 73.88% (Exelient & Firstchrome)

Directors Remuneration for FYE2021 (from gross profit 2019)

Datin Siah Li Mei: RM42k

Quek Wee Seng: RM577k

Quek Wee Seong: RM474k

Tajul Arifin: RM42k

Lim See Tow: RM42k

Total director remuneration: RM1.177 mil or 6.05%

Key Management Remuneration for FYE2021 (from gross profit 2019)

Tan Ley Wun: RM150k-200k

Khoo Ai Lee: RM150k-200k

Ku Yong Yee: RM100k-150k

Wong Eng Chuan: RM200k-250k

Quek Yan Song: RM50k-100k

key management remuneration: RM0.65mil-0.9mil or 3.34-4.62%

Use of fund

Construction of building: 42.03%

Purchase of machineries: 9.42%

Repayment of borrowings: 13.77%

Working capital: 13.77%

Listing Expenses: 21.74%

Good thing is:

1. PE11.5 is acceptable fair value.

2. ROE above 15%.

3. Revneue continue increase over past 3 years.

4. Global work from home trend increase demand of furniture.

The bad things:

1. Top 5 major customer contribute over 50% of company revenue.

2. Debt is high.

3. Director & top management remuneration is over 10% from company gross profit.

4. Use 13.77% IPO fund to pay debt, & listing expenses is 21.74% of total IPO fund (this 2 item is less help to contribute business growth in futures)

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion)

The company choosen the right timing to IPO as global work from home increase demand of furniture, however Mobilia furniture is more focus on wood based furniture. The exstimated completion time for factory block B & C is 2022, we should see more revenue come in after 2 years time (unable to find out how many % increase in production capacity). Please refer below chart to understand the risk vs business growth forecast for the company within 3 years.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.

Leveraging Cold Chain Logistics Visibility for COVID-19 Vaccines

Let's explore the logistics case study of one of the world’s largest pharma companies, the story of how this US-headquartered, globally present pharma giant improved teamwork in their logistics and is now confidently shipping COVID-19 vaccines using cold chain logistics visibility.

HPP Holdings Berhad

Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Open to apply: 15/12/2020

Close to apply: 07/01/2021

Listing date: 20/01/2021

Share Capital

Market Cap: RM139.8345mil

Total Shares: 388.43mil shares (Public apply: 19.4216mil, Company Insider/Miti/Private Placement/other: 89.2474mil)

Industry

Printing Industry CAGR 2016-2019: 6.04%

Top Five Industry Player (by PAT Margin)

Kinta Press & Packaging S/B: 20.98%

GL Printing S/B: 18.99%

Thumbprints Utd S/B: 13.47%

Hin Press S/B: 9.10%

Hayan Group (HPP): 8.72%

Business

Printing & production of paper-based packaging.

*Standard format machine utilisation rate 88.44%

*Currently 6 machines (5 in production line, 1 for training purpose)

*IPO add 2 machines (will dispose on old machines)

*Forecast printing capacity increase 20%

Revenue from Malaysia: 72.44%

Revenue from Oversea: 27.56%

Fundamental

1.Market: Ace Market

2.Price: RM0.36 (EPS:0.0212)

3.P/E: PE16.98

4.ROE(Pro Forma III): 8.885%

5.ROE: 12.72%(2020), 22.76%(2019), 28.82%(2018)

6.Cash & fixed deposit after IPO: RM0.0878 per shares

7.NA after IPO: RM0.25

8.Total debt to current asset after IPO: 0.4655 (Debt: 28.566mil, Non-Current Asset: 66.417mil, Current asset: 61.360mil)

9.Dividend policy: 20% Net profit dividend payout ratio policy.

Past Financial Performance (Revenue, EPS)

2020: RM101.203 mil (EPS: 0.0212)

2019: RM82.681 mil (EPS: 0.0343)

2018: RM64.395 mil (EPS: 0.0384)

Net Profit Margin

2020: 8.71%

2019: 16.53%

2018: 23.19%

After IPO Sharesholding

Aurora Meadow S/B: 51.72%

Kok Hon Seng: 5.94% (indirect 55.3%)

Lau Teee Tee @ Lau Kim Wah: 1.98% (indirect 53.51%)

Ng Soh Hoon: 3.58% (indirect: 57.66%)

Chong Fea Chin: 1.79% (indirect 53.7%)

Ang Poh Geok: 7.01%

Lau Tee Tee @ Lau Kim Wah: RM100k

Kok Hon Seng: RM0.954 mil

Ng Soh Hoon: RM0.216 mil

Philip Goh Teck Siang: RM60k

Choo Chee Beng: RM36k

Lee Chong Leng: RM36k

Total director remuneration: RM1.402 mil or 6.77%

Key Management Remuneration for FYE2020 (from gross profit 2019)

Tan Kian Siong @ Chen Kian Siong: RM0.251mil-0.3 mil

Mah Chen Wah: RM0.151mil-0.2mil

Ng Soh Moy: RM0.151mil-0.2mil

Teng Tiang Chia: RM0.201mil-0.25mil

Lee Kuei Yong: RM0.051mil-0.1mil

Subramaniam A/L Mogan: RM0.101mil-0.15mil

Nur Syafiqah Binti Hassan: RM0-0.05mil

key management remuneration: RM0.906mil-1.25mil or 4.38%-6.04%

Use of fund

Capital expenditure and expansion: 40.82%

Repayment of bank borrowing: 24.38%

Working capital: 16.31%

Sales and marketing expenses: 6.27%

Listing Expenses: 12.22%

Good thing is:

1. PE 16.98 under acceptable range.

2. Revenue increase over 3 years.

3. Major sharesholder hold by Aurora Meadow S/B, will have less large dispose of shares activities after IPO.

4. After IPO forecast printing capicity increase 20%.

The bad things:

1. ROE & EPS dropping over 3 years.

2. 16.31% IPO fund allocate to pay back bank borrowing.

3. Industry CAGC is not in high growth.

4. HPP is not major market player among their competitors.

5. Director & top management remuneration is over 10% of the company gross profit.

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion)

The IPO is at fair value.Estimated after completed install the new printing machine will have increase of printing capacity 20% that will increase revenue. However the business is not going to increase 100% in one or two years, as revenue also need to come with printing capacity. We might not see very high growth of business. (WARNING: business growth is not shares price growth)

for Risk vs business growth potential please refer below chart.

Mr D.I.Y Group (M) Berhad

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Open to apply: 06/10/2020

Close to apply: 14/10/2020

Listing date: 26/10/2020

Share Capital

Market Cap: RM294.95mil

Total Shares: 6.2766 mil shares (Public apply:125.532mil, Company Insider/Miti/Private Placement/other: 815.958mil)

Home Improvement Retail Sector.

Hardware store.

Malaysia: 670 stores. (Penisular: 568, East Malaysia:102)

Brunei: 4 stores.

Fundamental

1.Market: Main Market

2.Price: RM1.60 (EPS:0.0506)

-If retail IPO price lower than RM1.60, will refund the price difference.

3.P/E: PE31.6

4.ROE(Pro Forma III): 33.53

5.ROE: 54.19(2019), 58.79(2018), 60.14(2017)

6.Cash & fixed deposit after IPO: RM0.00807 per shares

7.NA after IPO: RM0.11

8.Total debt to current asset after IPO: 1.656 (Debt: 1.1203bil, Non-Current Asset: 1.1328bil, Current asset: 0.6767bil)

9.Dividend policy: 40% Net profit dividend payout ratio policy.

2020 (6-mth): RM1.051bil (EPS: 0.0190)

2019: RM2.275bil (EPS: 0.0522)

2018: RM1.771bil (EPS: 0.0506)

2017: RM1.229bil (EPS: 0.0345)

***prospectures book EPS using Pre-IPO 6.088bil shares to calculate EPS, pg211)

2020: 11.0%

2019: 14.0%

2018: 17.4%

2017: 17.1%

After IPO Sharesholding

1.Bee Family Limited: 50.6%

- Tan Yu Yeh

- Tan Yu Wei

- Yeh Family (PTC) LTD

- WEI Futures Capital

2.Hyptis: 15.2%

- Creador III L.P.

- Creador II, LLC

3.Platinum Alphabet: 6.9%

- Gan Choon Leng

- Tan Gaik Hoon

Directors Remuneration for FYE2020 (from gross profit 2019)

1.Dato' Azlam Shah Bin Alias: RM176k

2.Tan Yu Yah: RM1.187mil

3.Ong Chu Jin Adrian: RM1,271mil

4.Brahmal A/L Vasudevan: -

5.Ng Ing Peng: RM119k

6.Leng Choo Yin: RM111k

7.Tan Yu Wei: RM1.006mil

8.Soo Sze Yang: -

Total director remuneration from PBT: RM2.9646 mil or 0.308%

Key Management Remuneration for FYE2020 (from gross profit 2019)

1.Lim Chen Hwee: RM550k-600k

2.Tan Yew Hock: RM400k-450k

3.Tan Yew Teik: RM350k-400k

4.Hoe Lye Peng: RM450k-500k

5.Lau Boon Teck: RM450k-500k

6.Chin Guangui: 450k-500k

key management remuneration from PBT: RM2.65mil-2.95mil or 0.306%

Use of fund

1.Repayment of bank borrowing: 91.6%

2.Listing Expenses: 8.4%

Good thing is:

1. ROE over 15.

2. Most large in number of hardware store in Malaysia (cost advantage) & Brands influence.

3. Past 3 year revenue increasing.

4. total Director & key management fee did not over gross profit 3%.

5. Have fixed dividend payout policy.

The bad things:

1. PE31.6 is not cheap.

2. Net asset RM0.11

3. Net profit margin decreasing for pass 3 years.

4. 91.6% IPO fund use to pay back bank borrowing.

5. After IPO, still have RM1.12mil debt, but cash is RM50.623 mil.

This businees model successfully expand their business to almost whole Malaysia. But we cannot expect the business continue growth as past few years, as it already expand notion wide.

In the prospectus book Pg13 mention they expected to add additional 100 store in 2020 & 100 store in 2021, however did not mention the expected area to expand.

The price PE31.6 is included & price in potential of futures expansion, trust this is not a fair price & there might have opportunities to buy open market when it adjusted into their fair value.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.

Latest Intelligence