Tag: freight

Breaking News

How Can The Market Be at An All Time High and There Be A Freight Recession – Part II

In my previous post I outlined why I believe freight is slowing. Certain signals in the marketplace are telling us employment adds are decreasing, inventories are increasing and the PMI is decreasing. All of these are signs of a slowing economy. (For the record, I do not believe by any stretch the economy will contract - it is just we should not get used to GDP growth rates of 3% into the future). This slowing has resulted in less loads per truck and prices going down.

So, how can the stock market be hitting an all time high? I believe it is due to 3 reasons (Warning, I know a lot more about freight than I do about investing but here goes):

This chart compares the Dow Jones Transportation Index to the DJ30 and the S&P500. This is a one year return graph and ends on June 21. As of June 21, the DJ30 is up 6.66%, the SPX is up 7.1% and yet the DJT is DOWN 3.91% Bottom line is investors are shunning transports yet still embracing the overall economy. Why?

The Alternative Investment:

Investors are going to invest. That is what they do and they have two macro alternatives. First, they can invest in the "risk" markets (i.e., stocks) or they can invest in what is generally considered the "risk free" or "near risk free" investment. I will use the 10yr as a proxy for this second grouping. What we have seen recently is not only a 10 year treasury at multi year lows but we are also hearing the Fed discussing lowering the rates even further. This will drive investment dollars away from the "risk free" and into the markets.

It is no coincidence towards the end of last year when the Fed was not only raising rates but also calling for 3 rate hikes in 2019 the stock market tanked. Investors were deciding to move away from risk assets as the risk free was looking pretty good. Not so much any more as the 10yr is now bouncing around the 2% level.

The graph to the left is the graph of the 10 year treasury rates as of Friday, June 21. This movement of rates down has caused money to flow back into the risk asset markets and specifically look at the major move down since mid May. This is when the Fed made it pretty clear the only action they likely will take is a move down in rates.

The graph to the left is the graph of the 10 year treasury rates as of Friday, June 21. This movement of rates down has caused money to flow back into the risk asset markets and specifically look at the major move down since mid May. This is when the Fed made it pretty clear the only action they likely will take is a move down in rates.

% of The Economy Which Does Not Have Anything to Do with Shippable Goods:

This one is a bit nuanced. Let's just look at 30 years ago and think about what it meant for the economy to be growing at 3%. It was intuitive that the growth had to have much to do with autos, real hard electronics, housing etc. etc. These are all very "hard" goods which drove the economy.

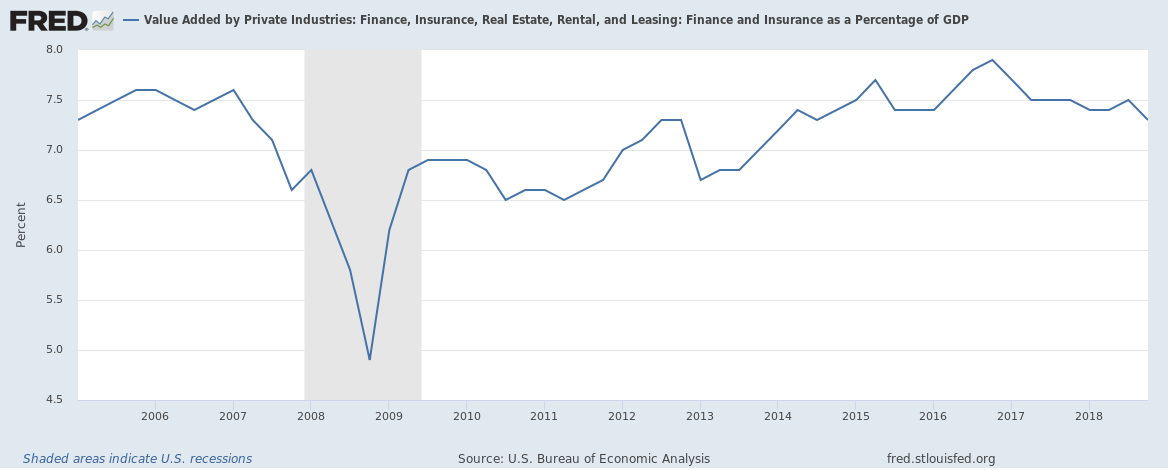

Today, when we the economy grows at 3% more of it has to do with finance, services and the infamous FANG stocks (Facebook, Amazon, Netflix and Google - Alphabet). Only one of these, Amazon, ships anything. The rest make their money in the "virtual" world. Very important to the economy but not so important to trucking. The graph below illustrates this:

The inverse of this graph is to ask how much of GDP is due to MFG:

So, how can the stock market be hitting an all time high? I believe it is due to 3 reasons (Warning, I know a lot more about freight than I do about investing but here goes):

- The alternative investment (10yr as a proxy)

- % of the economy which has nothing to do with goods

- The Fed.

What is happening:

Let me start off by showing what is actually happening:

This chart compares the Dow Jones Transportation Index to the DJ30 and the S&P500. This is a one year return graph and ends on June 21. As of June 21, the DJ30 is up 6.66%, the SPX is up 7.1% and yet the DJT is DOWN 3.91% Bottom line is investors are shunning transports yet still embracing the overall economy. Why?

The Alternative Investment:

Investors are going to invest. That is what they do and they have two macro alternatives. First, they can invest in the "risk" markets (i.e., stocks) or they can invest in what is generally considered the "risk free" or "near risk free" investment. I will use the 10yr as a proxy for this second grouping. What we have seen recently is not only a 10 year treasury at multi year lows but we are also hearing the Fed discussing lowering the rates even further. This will drive investment dollars away from the "risk free" and into the markets.

It is no coincidence towards the end of last year when the Fed was not only raising rates but also calling for 3 rate hikes in 2019 the stock market tanked. Investors were deciding to move away from risk assets as the risk free was looking pretty good. Not so much any more as the 10yr is now bouncing around the 2% level.

% of The Economy Which Does Not Have Anything to Do with Shippable Goods:

This one is a bit nuanced. Let's just look at 30 years ago and think about what it meant for the economy to be growing at 3%. It was intuitive that the growth had to have much to do with autos, real hard electronics, housing etc. etc. These are all very "hard" goods which drove the economy.

Today, when we the economy grows at 3% more of it has to do with finance, services and the infamous FANG stocks (Facebook, Amazon, Netflix and Google - Alphabet). Only one of these, Amazon, ships anything. The rest make their money in the "virtual" world. Very important to the economy but not so important to trucking. The graph below illustrates this:

|

| Non Shipment Economy |

Both of these graphs tell the same story. GDP can grow at a high rate and not have shippable product tendered to carriers. - Economy grows yet a freight recession sets in.

The Fed

What else can I say? The Fed has made a huge 180 degree turn around in the last few months and whether that is due to political pressure or real economics I will leave it to the real economists to figure out. But, reality is, the Fed has signaled rates are going down and they have somewhat backed themselves into a corner as it would be outright lying if they did not do this. This means more money will continue to go into inflating the asset bubble and less money will go into bonds.

I hope I have now explained (sorry for the two part length) why the freight recession likely will continue however the economy, as measured by the markets and GDP, will continue to do quite well.

Summary:

- Economy is slowing

- Investors have to invest in the market to get any kind of return due to the "risk free" paying so low.

- Investors are shunning the transports

- This drives the market to records

- Less and less of the GDP has to do with "shippable goods"

This is a link to Part 1 of this posting (for those reading on a reader)

How Can The Market be at All time High and There Be a “Freight Recession”? – PART I

The question posed in the title can be a perplexing problem and I am sure is of interest to both those who make a living running trucking companies as well as those who invest in them. If the market is a forward looking index (like they teach you on school) then the fact it has bid up stock prices would indicate it believes the economy is "booming" and if the economy is "booming" then there must be a lot of freight moving. I will attempt to explain why this connection (Market to freight volumes) is no longer true.

There will be two parts to this posting. The first will be to show the macroeconomic data I look at which tells me the freight market is slowing. The second part will be to show how the stock market could hit an all time high while the freight market slows.

There are 3 real reasons why the market (i.e., the SP500 and the Dow) is disconnected from what we, the "transporters of freight" see in the market:

While employment is incredibly robust and generally "all is good" there are some signs of cracks:

There will be two parts to this posting. The first will be to show the macroeconomic data I look at which tells me the freight market is slowing. The second part will be to show how the stock market could hit an all time high while the freight market slows.

There are 3 real reasons why the market (i.e., the SP500 and the Dow) is disconnected from what we, the "transporters of freight" see in the market:

- The alternative investment (i.e., 10yr).

- The % of the economy which has nothing to do with "goods".

- The Fed

Before I address each one, let's look at the data which supports why there is a "freight recession". For this I look at 3 different indices. First, my favorite, the "Total Business: Inventory to Sales Ratio" (St. Louis Fed). This measures how much activity is being used just to build inventories and the assumption is companies will not build inventories forever. When they stop building, the freight stops. Here is what the graph looks like back to 2015:

|

| Inventory to Sales Ratio - St. Louis Fed |

This graph clearly indicates (looking at the boom and bust cycles) inventories decrease then, in a recession, they increase. The shaded areas above are key recessions. You can see leading up to 2016 the economy was slow and it actually was close to the peak of the 2001 recession in 2016. Then came the "sugar high" of expectations and tax cuts and the inventory was burning down until close to the end of last year. Since then, the economy has been building inventory. Not a good sign for the economy overall but more importantly, for this blog, not important for the freight industry. I feel like I should not have to say this however just to be clear, companies do not build inventory forever. So, even if freight does not slow immediately there would be a clear expectation from the rational investor that freight will slow. Freight has slowed.

Second, let's look at the PMI trends. As a reminder, the PMI (Purchasing Manager's Index) generally gives you a look at whether the economy is expanding or not. A reading of 50 or above is generally good and below that is contraction. The index I like to look at is the MFG PMI:

|

| MFG PMI - Tradingeconomics.com |

I do not think I need to explain what is happening here suffice to say the decrease started around December of 2018 and has accelerated since then.

Since so much of the freight indices are tied up in hauling manufactured goods it is no doubt looking at this chart that there would be far less freight to haul and far fewer loads per truck then we would like.

The final piece of economic information is our labor force and the net change for employment. For this, I like to use a 3 month net change from the bureau of labor statistics. Why 3 months? Because BLS adjusts the previous two months as they get better data so by going to a 3 month net change you take into account most of the adjustments.

While employment is incredibly robust and generally "all is good" there are some signs of cracks:

|

| 3 Month Net Change in Employment - BLS |

While there is still net positive adds what this is showing is the net positive is slowing quite a bit. Could be we have just run out of workers or it could be, based on the data above, employers are starting to be very cautious about adding any more employees.

To give you an example of this, the last three months (Mar, Apr, May 2019) readings were 521, 433(p), 452(p) (p - preliminary readings) respectively. All three of those were below the lowest reading measured in 2018 which was 565 (January 2018). Another indication of a slowing economy.

Ok, so, the bottom line for this PART I is clearly the economy is starting to slow. Not in a recession (yet) but clearly slowing. I have opinions on why and I will leave those to myself but this is why you are seeing the FED not only not increasing rates but the conversation is now about lowering rates.

Stay tuned for PART II which will discuss the 3 reasons why the market, even though all these indicators show a slowing, hit new highs.

Latest Intelligence