Mortgage interest costs have undergone a “dramatic” surge over the past year, having risen by nearly 70% as of the first quarter, according to Statistics Canada.

Since the previous quarter alone, mortgage interest costs are up by 12.6%.

The data were released as part of StatCan’s Q1 national balance sheet and financial flow accounts. These figures represent the increase in interest costs in dollar terms, which is different from StatCan’s per capita measure included in the monthly inflation data, which is up nearly 30% year-over-year.

The report also revealed that the share of mortgages with an amortization period of longer than 25 years has risen sharply to 48.2%. That’s up from 46% a year ago and 37% in Q1 2021.

Mortgage debt posts slowest growth in 20 years

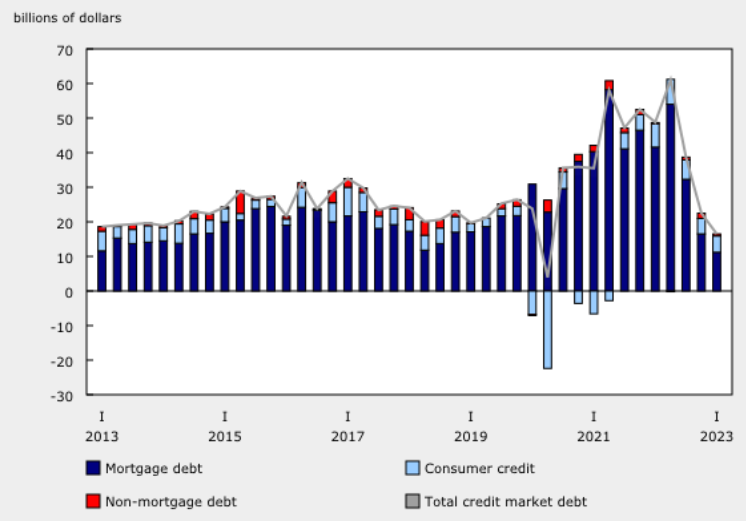

As further proof that high interest rates are weighing on real estate, total mortgage debt in Canada grew by just $11.2 billion in the first quarter, marking the smallest increase in 20 years.

This was the second straight quarter of slower mortgage borrowing growth, following growth of $16.5 billion in Q4, according to data released this week by Statistics Canada.

The results are down sharply from the record mortgage borrowing that took place over the past two years. The all-time record for mortgage borrowing was reached in Q2 2021 when consumers added $58.2 billion worth of mortgage debt.

The slowdown in Q1 comes despite an uptick in real estate activity in the early part of the year, and as the Bank of Canada continued to increase mortgage rates in January (and again more recently in June).

Household credit market debt (seasonally adjusted)

Other mortgage and real estate highlights

Other highlights from the latest quarterly report include:

- Household wealth grew by $520 billion (+3.4% from Q4)

- This was bolstered by a 3.2% (+$243.6 billion) increase in residential real estate values. This followed three straight quarters of declines in 2022 that caused real estate wealth to fall by 10.1% (-$849.3 billion)

- The debt-service ratio (total household debt payments relative to personal disposable income) rose 14.9%

- Debt payments were up 3.3% quarter-over-quarter

- Obligated principal payments fell 6.8% “as the significant stock of variable rate mortgages likely allowed interest payments to further adjust without a concomitant rise in principal”

- Fixed-payment variable rate mortgages accounted for nearly 25% of all outstanding chartered bank mortgages

Debt-servicing costs expected to rise further

Even though overall debt growth slowed, the debt-service ratio continued to rise while debt repayment slowed.

That trend is expected to continue over the course of the year and peak by the second half of 2024 “as interest rates are now expected to rise and remain elevated for longer,” according to Maria Solovieva of TD Economics.

“This will create additional headwinds for households with a high sensitivity to interest rates (such as variable rate mortgage holders) and could result in higher delinquency rates in the future,” she noted, pointing to a rise in missed payments revealed in Equifax Canada’s first-quarter credit trends report.

“This is a relatively new trend as in 2022 delinquencies were more pronounced among consumers without mortgages,” she added. “The Bank of Canada will need to maintain a close watch on household credit performance as higher interest rates continue to weigh on Canadian households this year.”

- SEO Powered Content & PR Distribution. Get Amplified Today.

- EVM Finance. Unified Interface for Decentralized Finance. Access Here.

- Quantum Media Group. IR/PR Amplified. Access Here.

- PlatoAiStream. Web3 Data Intelligence. Knowledge Amplified. Access Here.

- Source: https://www.canadianmortgagetrends.com/2023/06/mortgage-interest-costs-surge-by-nearly-70-in-the-past-year/