Mark your calendars for the ultimate real estate experiences with Inman’s upcoming events! Dive into the future at Connect Miami, immerse in luxury at Luxury Connect, and converge with industry leaders at Inman Connect Las Vegas. Discover more and join the industry’s best at inman.com/events.

Plummeting commercial real estate values may prompt New York Community Bancorp to tap a more stable asset to shore up its balance sheet: residential mortgages originated when interest rates were low.

New York Community Bancorp (NYCB) is looking to pledge about $5 billion in home loans originated by Flagstar Bank as backing for a “synthetic risk transfer” that would bolster its capital reserves, Bloomberg reported Wednesday, citing anonymous sources with knowledge of the talks.

NYCB, which acquired Flagstar Bank 2022, is one of a number of regional lenders that could need fresh capital if the performance of loans they made to commercial developers continues to deteriorate. With office and retail vacancies remaining elevated in many markets after the pandemic, the properties that served as collateral for the loans are, in some cases, worth less than the outstanding balance on loans.

Since reporting a $252 million fourth-quarter loss on Jan. 31, NYCB shares have lost more than half their value. Shares in the bank, which hit a 52-week high of $14.22 on July 28, briefly touched a 52-week low of $3.60 Wednesday before climbing back above $4.

In reporting earnings, NYCB said it boosted its provision for credit losses by 533 percent, to $833 million. Fourth quarter charge-offs of $117 million in multifamily and $42 million in commercial real estate loans also sounded alarm bells with investors. Those concerns were amplified when Fitch Ratings and Moody’s Investors Service downgraded NYCB’s credit ratings, which could make it more costly for the bank to borrow money.

“In terms of financial strategy, the bank is seeking to build its capital but just took an unanticipated loss on commercial real estate which is a significant concentration for the bank,” Moody’s analysts said Tuesday.

Moody’s analysts said they were also concerned about the departure of NYCB’s chief risk officer, Nick Munson, and chief audit officer, Meagan Belfinger, who left the company unannounced before earnings were released.

After the ratings downgrade, NYCB announced Wednesday that it was appointing former Flagstar Bank President and CEO Sandro DiNello as executive chairman. DiNello, who was formerly non-executive chairman, will “work alongside” the executive who spearheaded the Flagstar merger, NYCB President and CEO Thomas Cangemi, “to improve all aspects of the bank’s operations.”

Cangemi announced Wednesday that NYCB is in the process of bringing in a new chief risk officer and chief audit executive with large bank experience, “and we currently have qualified personnel filling those positions on an interim basis.”

In an attempt to reassure investors and clients, NYCB also publicized that its deposits have continued to grow this year, to $83 billion, and that its $37.3 billion in total liquidity exceeds uninsured deposits of $22.9 billion.

While NYCB’s share price has stabilized, Morningstar DBRS joined Fitch and Moody’s in downgrading the bank’s credit ratings Thursday.

“At $37.3 billion, liquidity appears sufficient, but given the bank failures last spring, we remain cautious given that the adverse headline risk, including a significant decline in NYCB’s stock price, could eventually spook customer and depositor confidence,” Morningstar DBRS analysts said.

Last year’s failures of Silicon Valley Bank, Signature Bank and First Republic Bank — largely driven by rising interest rates — put regional banks under heightened scrutiny by ratings agencies.

NYCB claims to be the second-largest multifamily residential portfolio lender in the country, and the leading multifamily lender in the New York City market area, specializing in rent-regulated, non-luxury apartment buildings.

“NYCB’s core historical commercial real estate lending, significant and unanticipated loss on its New York office and multifamily property could create potential confidence sensitivity,” Moody’s analysts said in downgrading NYCB’s credit ratings to junk status. “The company’s elevated use of market funding may limit the bank’s financial flexibility in the current environment.”

Former FDIC Chair Sheila Bair told Yahoo Finance Thursday that most multifamily housing — which is included in the commercial real estate category — is actually “a good place to be. But in certain pockets, particularly in New York, where we have some pretty restrictive rent control laws, you’re seeing some distress.”

Bair said that while it’s important not to “taint the entire sector,” there are problems in segments of CRE including urban office and some urban retail. Many regional banks “do have heavy exposure to distressed parts of the market and they’re gonna need to work through that.”

“Hopefully, they reserved enough,” Bair said. “But we’ll see. If they don’t, we’re gonna have probably a few more bank failures. But it’s nothing like what we saw during 2008.”

Appearing on 60 Minutes Sunday, Federal Reserve Chair Jerome Powell said that while he doesn’t expect a repeat of the 2008 financial crisis, “there will be some banks that have to be closed or merged out of existence because of this. That’ll be smaller banks, I suspect, for the most part.”

The latest worries over commercial real estate values could make jumbo mortgages costlier and harder to come by, since regional banks have traditionally been a leading provider.

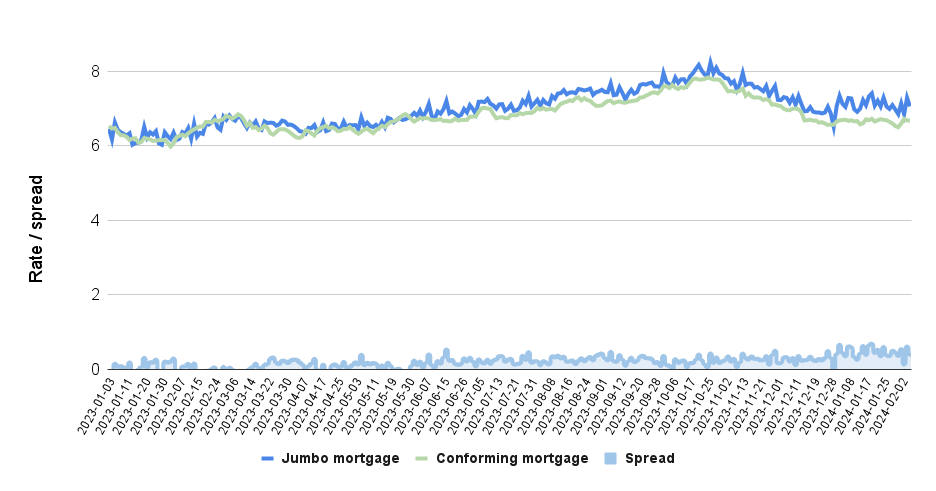

According to daily rate lock data tracked by the Optimal Blue Mortgage Market Indices, the “spread” between rates for jumbo and conforming mortgages widened after the March 10, 2023 closure of Silicon Valley Bank — a trend that’s continued this year.

Widening conforming, jumbo mortgage ‘spread’

Historical spread between rates on jumbo and conforming mortgages. Source: Inman analysis of Optimal Blue rate lock data retrieved from FRED, Federal Reserve Bank of St. Louis.

“Unlike conforming loans, which are largely financed through mortgage-backed securities (MBS) via capital markets, the jumbo mortgage space is almost entirely funded via the banking sector, and some regional banks are more concentrated in jumbo mortgage lending than others,” Fannie Mae forecasters warned last March. “Ongoing liquidity stress could limit home financing and therefore sales in the related market segments and geographies with high jumbo concentration.”

During January and February of 2023, Optimal Blue data shows the spread between jumbo and conforming mortgages averaged about 1 basis point, with rates on jumbo mortgages at times lower than rates for conforming mortgages (a basis point is one hundredth of a percentage point).

During the remaining 10 months of 2023, from March through December, the spread averaged 19 basis points. So far this year, through Feb. 7, the spread has averaged 46 basis points — nearly half a percentage point.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.inman.com/2024/02/08/flagstar-mortgages-could-help-nycb-shore-up-its-balance-sheet/