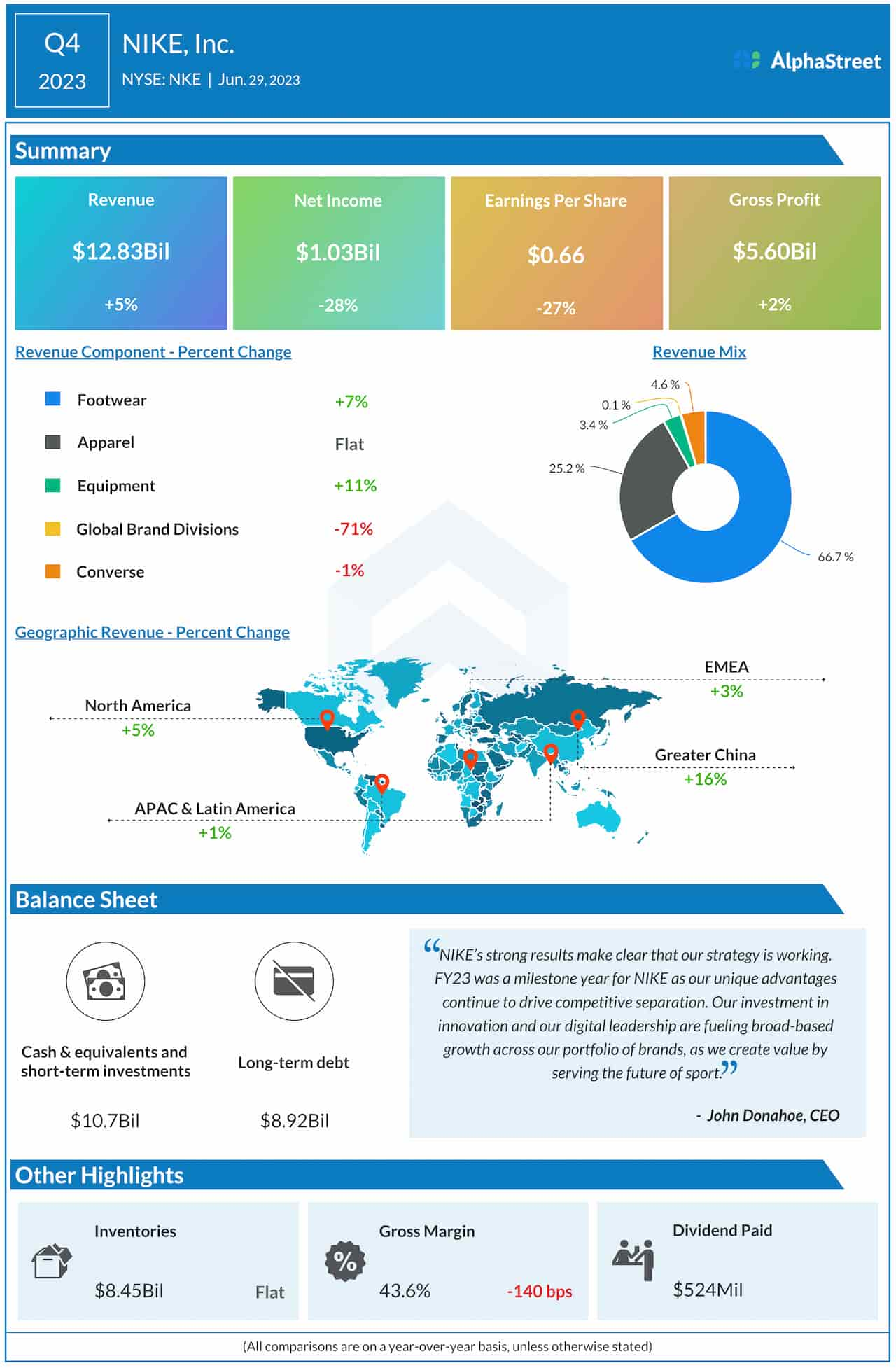

Sports apparel giant Nike, Inc. (NYSE: NKE) ended fiscal 2023 on a mixed note, reporting higher revenues that topped expectations and a decline in profit. The bottom line also fell short of analysts’ expectations, marking the first miss in nearly three years.

After slipping to a two-and-half-year low in the latter half of 2022, Nike’s stock has recouped a part of those losses but it mostly traded sideways this year. Investors were not impressed by the fourth-quarter numbers, and the stock slipped following the announcement last week. It has underperformed the S&P 500 index in recent years, reversing the long-term trend. Being one of the strongest and most valuable brands in the world, NKE has long been a favorite among investors, a trend that is likely to continue. Going by experts’ perdition, the stock is on its way to crossing the $130 mark in the next twelve months.

Sales Trend

Currently, the Beaverton-headquartered sneaker maker is focused on investing in innovation and ramping up digital capabilities as it targets to achieve sustainable and profitable sales growth in the new fiscal year. In the most recent quarter, Nike Direct sales grew an impressive 15%. Right now, the primary risk to profitability is inventory buildup, which often forces the company to push merchandise at discounted prices.

The margin pressure and muted consumer sentiment, due to financial uncertainties and cutback on discretionary spending, might remain a challenge for the business in the near future. However, recent sales trends indicate that consumers still have an appetite for Nike products despite the uncertainties, thanks to its band value.

“Our inventory is flat year-over-year in value and down in units versus 12 months ago. The actions we’ve taken position us for more profitable growth moving forward. Across our business, we continue to build a marketplace that addresses how consumers want to be served giving them what they want when they want it and how they want it. NIKE creates distinction across the marketplace by segmenting consumer experiences to drive deep direct connections with consumers and grow the marketplace,” commented Nike’s CEO John Donahoe at the earnings call.

Mixed Q4

May-quarter earnings declined in double digits to $1.03 billion $0.66 per share from $1.44 billion or $0.90 per share last year. The latest number also came in below consensus estimates, which is the first miss in around three years. The bottom line was negatively impacted by lower margins, reflecting higher input and logistics costs.

Revenues, meanwhile, increased 5% annually to $12.83 billion and topped expectations. The growth is attributable to stronger demand in the core footwear segment. Sales rose across all geographical segments. The relaxation of COVID restrictions in China also contributed to the top-line growth.

Inventory increased from the pre-COVID levels, but was broadly unchanged year-over-year. The inventory pressure and weak unit sales have made the company revive certain wholesale partnerships which were discontinued a couple of years ago when it embraced the direct-to-consumer strategy.

Guidance

Taking a cue from the slowdown, the management issued cautious guidance forecasting flat-to-up-low-single-digits revenue growth for the first quarter. Full-year revenue is seen growing in mid-single digits, while gross margin is expected to rise in the range of 1.4 to 1.6 percentage points.

The post-earnings weakness of continued this week, and the stock traded lower in the early hours of Monday. It is down 7% since the beginning of the year.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Automotive / EVs, Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- BlockOffsets. Modernizing Environmental Offset Ownership. Access Here.

- Source: https://news.alphastreet.com/after-mixed-start-to-fy24-nike-expects-margin-pressure-to-persist/#utm_source=rss&utm_medium=rss&utm_campaign=after-mixed-start-to-fy24-nike-expects-margin-pressure-to-persist