Tag: tax

Breaking News

CTOS Digital Berhad

Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Open to apply: 30/06/2021

Close to apply: 06/07/2021

Balloting: 08/07/2021

Listing date: 19/07/2021

Balloting: 08/07/2021

Listing date: 19/07/2021

Share Capital

Market Cap: RM411.896 mil

Total Shares: 2,200 mil shares

Market Cap: RM411.896 mil

Total Shares: 2,200 mil shares

Industry (Net Profit %)

M'sia 2016-2020 CAGR: 12.9%

M'sia 2016-2025E CAGR: 12.7%

ASEAN 2016-2020 CAGR: 12.8%

ASEAN 2016-2025E CAGR: 11.4%

M'sia 2016-2020 CAGR: 12.9%

M'sia 2016-2025E CAGR: 12.7%

ASEAN 2016-2020 CAGR: 12.8%

ASEAN 2016-2025E CAGR: 11.4%

Competitors compare (EBITDA%)

CTOS: 36.9%

Experian: 24%

CBM: 13.9%

CTOS: 36.9%

Experian: 24%

CBM: 13.9%

Business

Credit bureaux in the ASEAN region

Malaysia: 94.8%

International B2B: 5.2%

Credit bureaux in the ASEAN region

Malaysia: 94.8%

International B2B: 5.2%

Fundamental

1.Market: Main Market

2.Price: RM1.10

*Institutional price to be determined

*If final price less then RM1.10, balance will be refund.

3.P/E: PE61.8 (EPS: 0.0178)

4.ROE(Pro Forma III): 13.18%

5.ROE: 32.81%(2020), 49.41%(2019), 49.40%(2018),

6.Cash & fixed deposit after IPO: 0.0264

7.NA after IPO: RM0.13

8.Total debt to current asset after IPO: 0.507 (Debt: 41.469mil, Non-Current Asset: 247.716mil, Current asset: 81.829mil)

9.Dividend policy: 60% profit after tax dividend policy.

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2020: RM141.496 mil (Eps: 0.0178),PAT%: 27.9%

2019: RM129.141 mil (Eps: 0.0177),PAT%: 30.2%

2018: RM110.465 mil (Eps: 0.0135),PAT%: 26.8%

1.Market: Main Market

2.Price: RM1.10

*Institutional price to be determined

*If final price less then RM1.10, balance will be refund.

3.P/E: PE61.8 (EPS: 0.0178)

4.ROE(Pro Forma III): 13.18%

5.ROE: 32.81%(2020), 49.41%(2019), 49.40%(2018),

6.Cash & fixed deposit after IPO: 0.0264

7.NA after IPO: RM0.13

8.Total debt to current asset after IPO: 0.507 (Debt: 41.469mil, Non-Current Asset: 247.716mil, Current asset: 81.829mil)

9.Dividend policy: 60% profit after tax dividend policy.

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2020: RM141.496 mil (Eps: 0.0178),PAT%: 27.9%

2019: RM129.141 mil (Eps: 0.0177),PAT%: 30.2%

2018: RM110.465 mil (Eps: 0.0135),PAT%: 26.8%

After IPO Sharesholding

Creador II: 40% (indirect)

Chung Tze Keong:4.5%

Chung Tze Wen: 4.5%

Creador II: 40% (indirect)

Chung Tze Keong:4.5%

Chung Tze Wen: 4.5%

Directors & Key Management Remuneration for FYE2021 (from gross profit 2020)

Total director remuneration: RM1.909mil

key management remuneration: RM3.25mil- 3.5mil

total (max): RM5.409 mil or 4.45 %

Total director remuneration: RM1.909mil

key management remuneration: RM3.25mil- 3.5mil

total (max): RM5.409 mil or 4.45 %

Use of fund

Repayment bank borrowing: 70.5%

Acquisition to be identified: 26.7%

Listing expenses: 2.8%

Repayment bank borrowing: 70.5%

Acquisition to be identified: 26.7%

Listing expenses: 2.8%

Highlight

1. Competitive advantage: limited number of player able to offer the full suite of digital solutions in Malaysia.

2. Market share in 2020 (Malaysia): 71.2%

3. Expand to Philippines (2020 acquired 51% CIBI)

4. Expand to Thailand (2020 acquired 20% BOL)

1. Competitive advantage: limited number of player able to offer the full suite of digital solutions in Malaysia.

2. Market share in 2020 (Malaysia): 71.2%

3. Expand to Philippines (2020 acquired 51% CIBI)

4. Expand to Thailand (2020 acquired 20% BOL)

Good thing is:

1. High growth, high margin, Consistent ROE business.

2. Less competitors.

3. Revenue continue on growing.

4. Expand to other ASEAN countries.

5. Director & key management remuneration at acceptable category.

1. High growth, high margin, Consistent ROE business.

2. Less competitors.

3. Revenue continue on growing.

4. Expand to other ASEAN countries.

5. Director & key management remuneration at acceptable category.

The bad things:

1. High PE, at PE61.8

2. 70.5% IPO fund for repayment bank borrowing.

1. High PE, at PE61.8

2. 70.5% IPO fund for repayment bank borrowing.

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

Is a charging premium PE IPO, with PE61.8. If CTOS successful cases able to duplicate into other ASEAN countries, it will worth this price (if fail to duplicate their successful cases, investor need hold long period for return of capital).

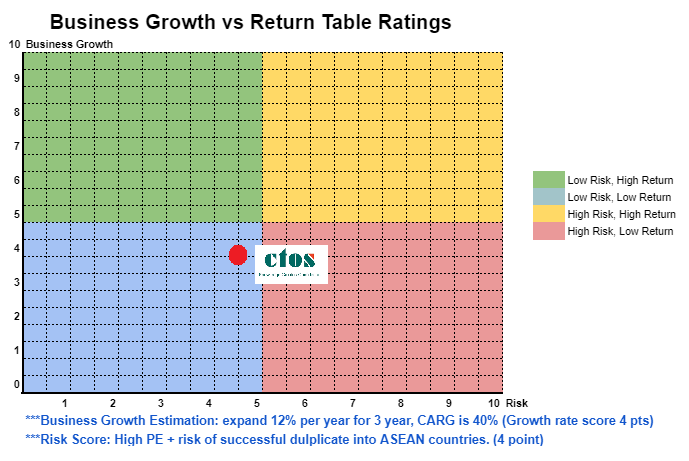

Futures 3 year estimation for business expansion & risk sorce, please refer to below chart.

Is a charging premium PE IPO, with PE61.8. If CTOS successful cases able to duplicate into other ASEAN countries, it will worth this price (if fail to duplicate their successful cases, investor need hold long period for return of capital).

Futures 3 year estimation for business expansion & risk sorce, please refer to below chart.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.

Latest Intelligence