Last week, public software markets suffered significant compression. MongoDB fell 24%; UIPath fell 36% ; Salesforce fell 15% ; Workday was down 11%.

Weaker revenue projections tend to cause sell-offs.

These large drops aren’t unprecedented. In 2016, valuations fell 57%. Is it different this time?

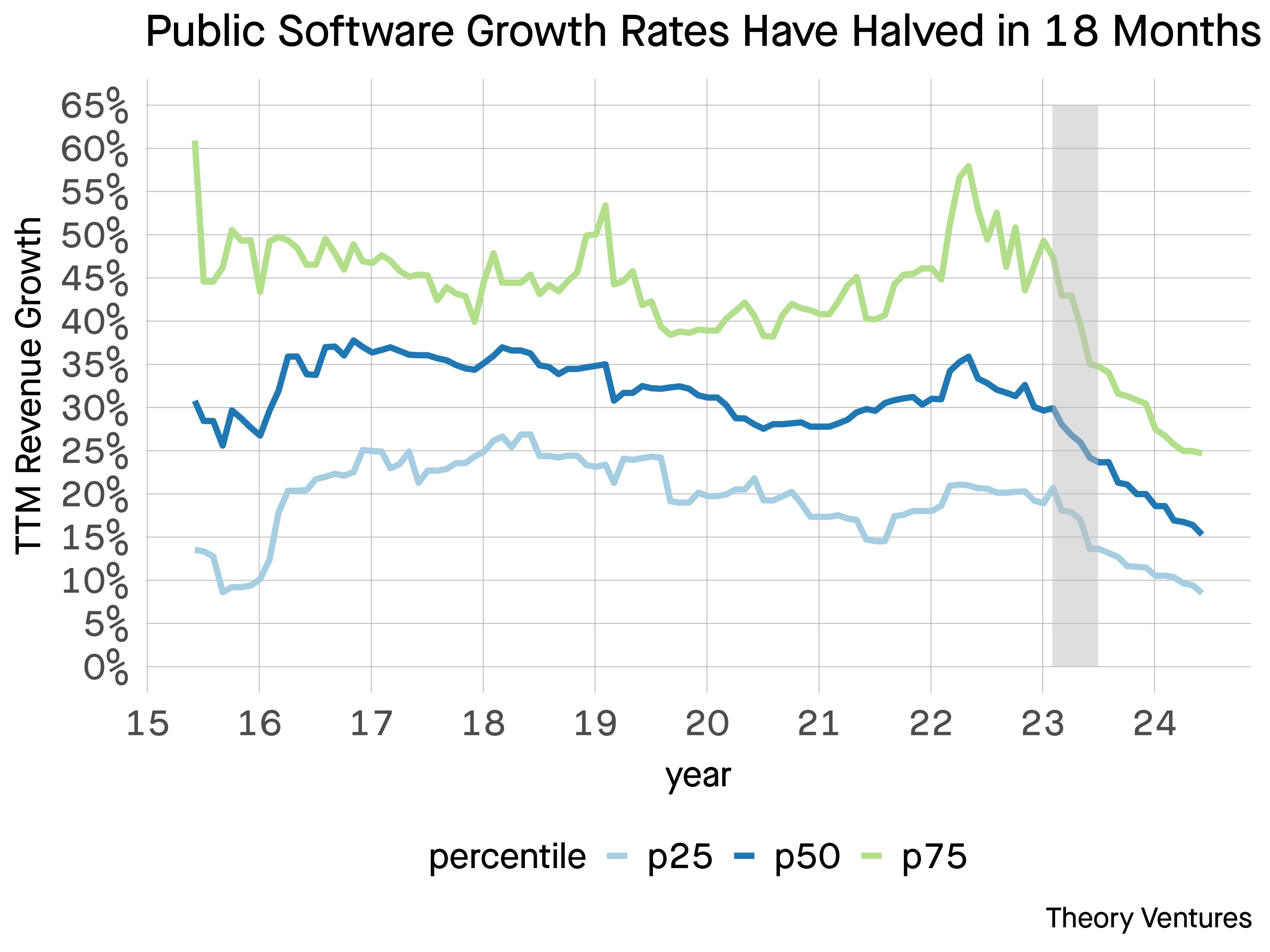

Growth rates have changed meaningfully. The 25th, 50th, & 75th percentiles for public growth rates have halved in the last 18-24 months. The grey bar indicates Covid ending & marks the beginning of the slide.

Each of these percentiles is now meaningfully lower than the average over the past decade.

Top quartile companies in 2024 grow at the same rates as bottom quartile companies in 2018.

Future revenue ramps have been the dominant driver of software valuations for the vast majority of the last decade. When they fall, valuations compress.

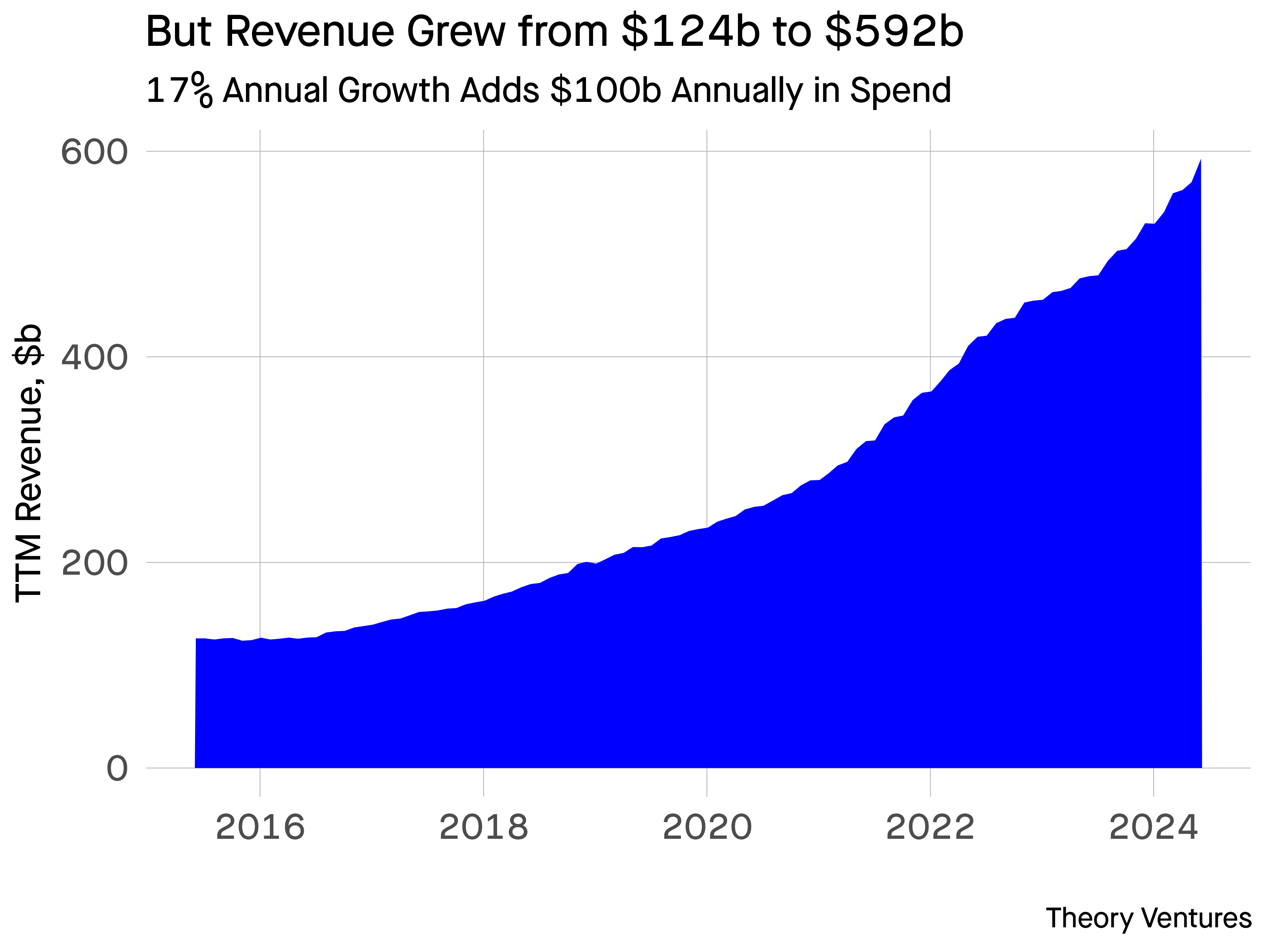

Some context is helpful : during the same period, total software revenue across the public companies grew from $124b to $592b. The overall market has ballooned.

In the last 12 months, public software companies will grow on average 17%, which will add $100b in revenue across these businesses.

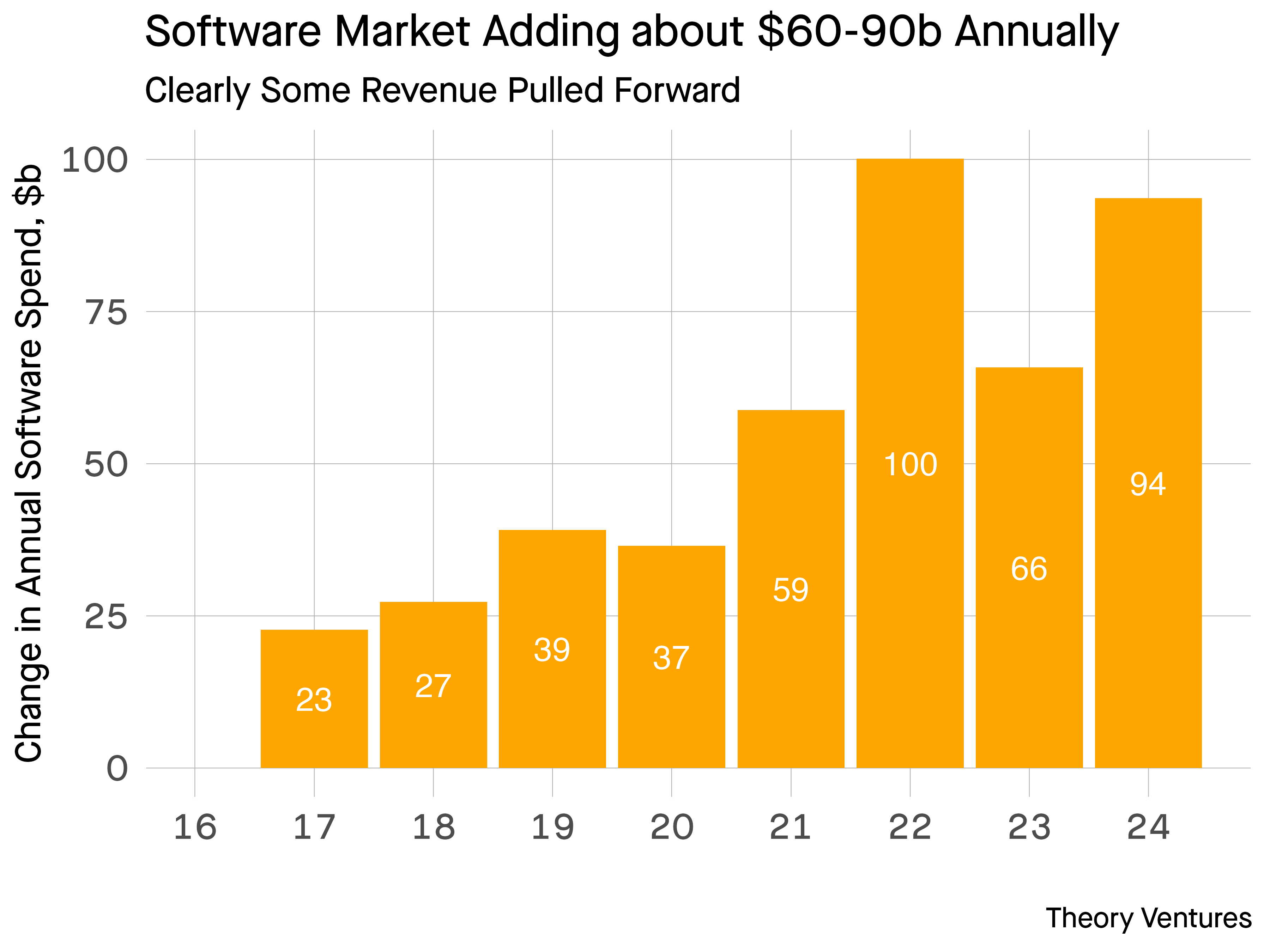

Looking at the changes in software revenue, we see that the market is on a straight line to surge past $100b. Covid catalyzed $100b in new software revenue bookings in 2022.

At a 6x revenue multiple, that’s $600b in market cap. There’s plenty of value creation to be seized.

But for many of the largest companies, the law of large numbers & the bigger bookings figures demanded by financial plans impose challenges. Salesforce has sustained double-digit revenue growth for two decades as a public company. With 150k+ customers, saturation is a challenge, despite a broad product suite to cross-sell.

With $35b in 2024 revenue, Salesforce’s 10% revenue growth target is $3.5b net new bookings – equivalent to adding Atlassian’s or Crowdstrike’s entire revenue this year.

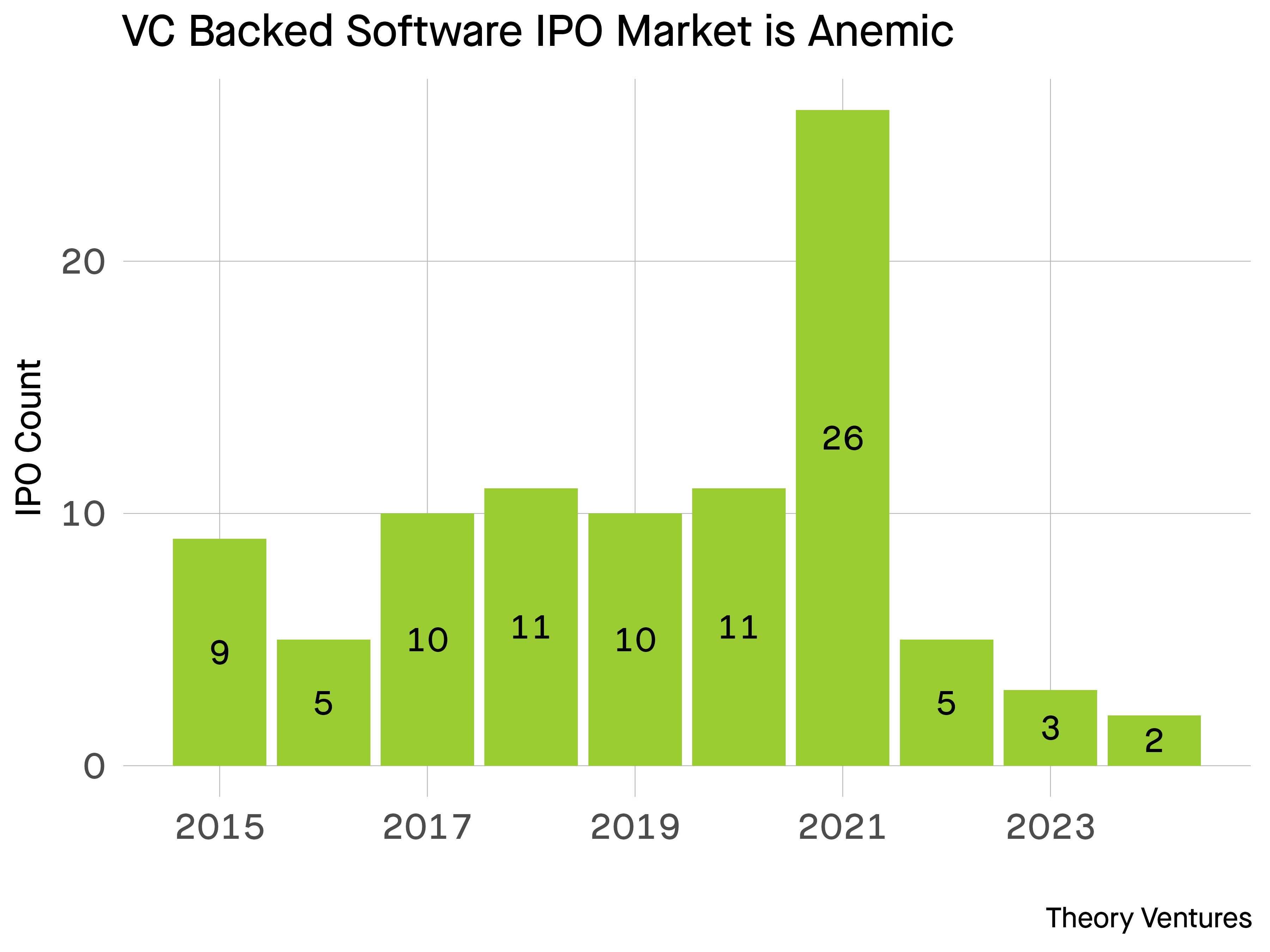

Also, the average age of these companies is now 20 years old since founding. The lack of software backed IPOs in the last few years aside from one or two exceptions has meant the old guard dominates these indices.

The average number of VC-backed software companies in the US in the last three years is less than a third of the average over the last decade.

Instead, the 40-60% wild horses grow in the private markets, absent from these figures.

Some of the older software companies are slowing – a natural part of the lifecycle. But it would be a mistake to extrapolate that to the entire market. The private markets hide the fastest growing companies.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.tomtunguz.com/weakness-in-software/