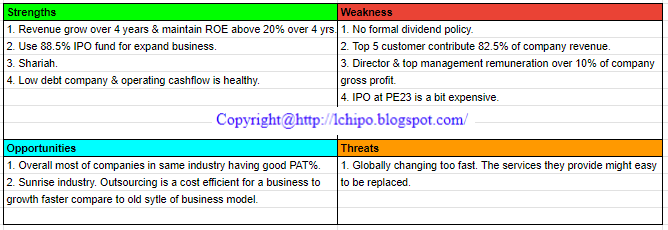

Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal

opinion and reader should take their own risk in investment decision.

opinion and reader should take their own risk in investment decision.

Open to apply: 21 Jun 2023

Close to apply: 11 July 2023

Balloting: 14 Jul 2023

Listing date: 26 Jul 2023

Close to apply: 11 July 2023

Balloting: 14 Jul 2023

Listing date: 26 Jul 2023

Share Capital

Market cap: RM144 mil

Total Shares: 480 mil shares

Market cap: RM144 mil

Total Shares: 480 mil shares

Industry CARG

Estimated Market Size and Growth Forecast for the GBS Industry in Malaysia, 2020-2027: 6.3%

Industry competitors comparison (PAT%)

Daythree: 9.6%

Scicom: 11.9% (PE12.06)

Aegis BPO Malaysia S/B: 17.4%

TDCX (MY) S/B: 19.9%

Teleperformance Malaysia S/B: 12.1%

Others (6 company) : 7.5% to 11.4%

Others (4 company): -62.17% to 2.2%

Estimated Market Size and Growth Forecast for the GBS Industry in Malaysia, 2020-2027: 6.3%

Industry competitors comparison (PAT%)

Daythree: 9.6%

Scicom: 11.9% (PE12.06)

Aegis BPO Malaysia S/B: 17.4%

TDCX (MY) S/B: 19.9%

Teleperformance Malaysia S/B: 12.1%

Others (6 company) : 7.5% to 11.4%

Others (4 company): -62.17% to 2.2%

Business (FYE 2022)

GBS services provider (Gobal Business Services) focusing on CX lifecycle management services (customer experience) enabled by in-house developed digital tools.

***for easy understanding, is a type outsourcing services company that focus on customer experience segment.

Customer Segment (FYE2022)

1.Energy & utilities: 48.9%

2.Telecommunications & media: 23.4%

3.Fintech & financial services: 15.4%

4.Construction: 3.8%

5.Others: 8.5%

GBS services provider (Gobal Business Services) focusing on CX lifecycle management services (customer experience) enabled by in-house developed digital tools.

***for easy understanding, is a type outsourcing services company that focus on customer experience segment.

Customer Segment (FYE2022)

1.Energy & utilities: 48.9%

2.Telecommunications & media: 23.4%

3.Fintech & financial services: 15.4%

4.Construction: 3.8%

5.Others: 8.5%

Fundamental

1.Market: Ace Market

2.Price: RM0.30

3.Forecast P/E: 23.1 @ EPS0.013

4.ROE(Pro Forma III): 11.01%

5.ROE: 23.60%(FYE2022), 34.12%(FYE2021), 29.43%(FYE2020), 24.68%(FYE2019)

6.Net asset: RM0.12

7.Total debt to current asset IPO: 30.92 (Debt: 19.639mil, Non-Current Asset: 12.874mil, Current asset: 63.521mil)

8.Dividend policy: no formal dividend policy.

9. Shariah status: Yes

1.Market: Ace Market

2.Price: RM0.30

3.Forecast P/E: 23.1 @ EPS0.013

4.ROE(Pro Forma III): 11.01%

5.ROE: 23.60%(FYE2022), 34.12%(FYE2021), 29.43%(FYE2020), 24.68%(FYE2019)

6.Net asset: RM0.12

7.Total debt to current asset IPO: 30.92 (Debt: 19.639mil, Non-Current Asset: 12.874mil, Current asset: 63.521mil)

8.Dividend policy: no formal dividend policy.

9. Shariah status: Yes

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2022 (FYE 31Dec): RM65.105 mil (Eps: 0.013),PAT: 9.6%

2021 (FYE 31Dec): RM58.133 mil (Eps: 0.020),PAT: 16.6%

2020 (FYE 31Dec): RM47.713 mil (Eps: 0.012),PAT: 11.8%

2019 (FYE 31Dec): RM37.463 mil (Eps: 0.008),PAT: 10.2%

2022 (FYE 31Dec): RM65.105 mil (Eps: 0.013),PAT: 9.6%

2021 (FYE 31Dec): RM58.133 mil (Eps: 0.020),PAT: 16.6%

2020 (FYE 31Dec): RM47.713 mil (Eps: 0.012),PAT: 11.8%

2019 (FYE 31Dec): RM37.463 mil (Eps: 0.008),PAT: 10.2%

Order Book/Contract

Currently have: 19 contract

– Renewable: 1 contract

– Non-renewable: 17 contract (RM66.7mil @ 5contract, 13contract by rendered)

– FYE2022 expired & renewed: 1 contract

Currently have: 19 contract

– Renewable: 1 contract

– Non-renewable: 17 contract (RM66.7mil @ 5contract, 13contract by rendered)

– FYE2022 expired & renewed: 1 contract

Operating cashflow vs PBT

2022: 83.39%

2021: 65.12%

2020: 56.55%

2019: 70.74%

2022: 83.39%

2021: 65.12%

2020: 56.55%

2019: 70.74%

Major customer (2022)

Client G: 29.0%

Client F: 19.9%

Client E: 18.4%

Client D: 10.3%

Client A: 4.9%

***total 82.5%

Client G: 29.0%

Client F: 19.9%

Client E: 18.4%

Client D: 10.3%

Client A: 4.9%

***total 82.5%

Major Sharesholders

Dayspring Capital: 36% (direct)

Paul Raymond Raj A/L Davadass: 36% (indirect)

Cloud Marshal: 23.1%

BLM Holdings: 15.4% (direct)

Thanos capital: 23.1% (indirect)

Gan Jhia Jhia: 23.1% (indirect)

Leong Kok Cheng: 23.1% (indirect)

Lee King Loon: 23.1% (indirect)

Bernadine Lee Siew Ling: 15.4% (indirect)

Dayspring Capital: 36% (direct)

Paul Raymond Raj A/L Davadass: 36% (indirect)

Cloud Marshal: 23.1%

BLM Holdings: 15.4% (direct)

Thanos capital: 23.1% (indirect)

Gan Jhia Jhia: 23.1% (indirect)

Leong Kok Cheng: 23.1% (indirect)

Lee King Loon: 23.1% (indirect)

Bernadine Lee Siew Ling: 15.4% (indirect)

Directors & Key Management Remuneration for FYE2023

(from Revenue & other income 2022)

Total director remuneration: RM1.275mil

key management remuneration: RM0.90mil – RM1.15mil

total (max): RM2.425 mil or 14.79%

(from Revenue & other income 2022)

Total director remuneration: RM1.275mil

key management remuneration: RM0.90mil – RM1.15mil

total (max): RM2.425 mil or 14.79%

Use of funds

1. Office expansion: 21.4%

2. Recruit industry experts to capture growth opportunities: 9.1%

3. Capital expenditure in networking infrastructure, IT hardware and software: 9.1%

4. Branding, marketing and promotional activities: 4.5%

5. Working capital: 44.4%

6. Estimated listing expenses: 11.5%

1. Office expansion: 21.4%

2. Recruit industry experts to capture growth opportunities: 9.1%

3. Capital expenditure in networking infrastructure, IT hardware and software: 9.1%

4. Branding, marketing and promotional activities: 4.5%

5. Working capital: 44.4%

6. Estimated listing expenses: 11.5%

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

Overall is a good IPO. Their IPO PE is a bit expensive, but the company is having fast growth performance.

Overall is a good IPO. Their IPO PE is a bit expensive, but the company is having fast growth performance.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- EVM Finance. Unified Interface for Decentralized Finance. Access Here.

- Quantum Media Group. IR/PR Amplified. Access Here.

- PlatoAiStream. Web3 Data Intelligence. Knowledge Amplified. Access Here.

- Source: http://lchipo.blogspot.com/2023/06/daythree-digital-berhad.html