“Advanced AI could represent a profound change in the history of life on Earth,” stated the Asilomar AI Principles in 2017, two years after the founding of OpenAI.

Fast forward to 2023, and its effects are already being recognized.

The introduction of generative AI into the tech ecosystem has opened out realms of opportunity, previously thought only to be the stuff of fiction. From chatbots to financial forecasting, the application of the technology is being both revered and feared, with even the founding fathers of Open AI calling for a pause in development.

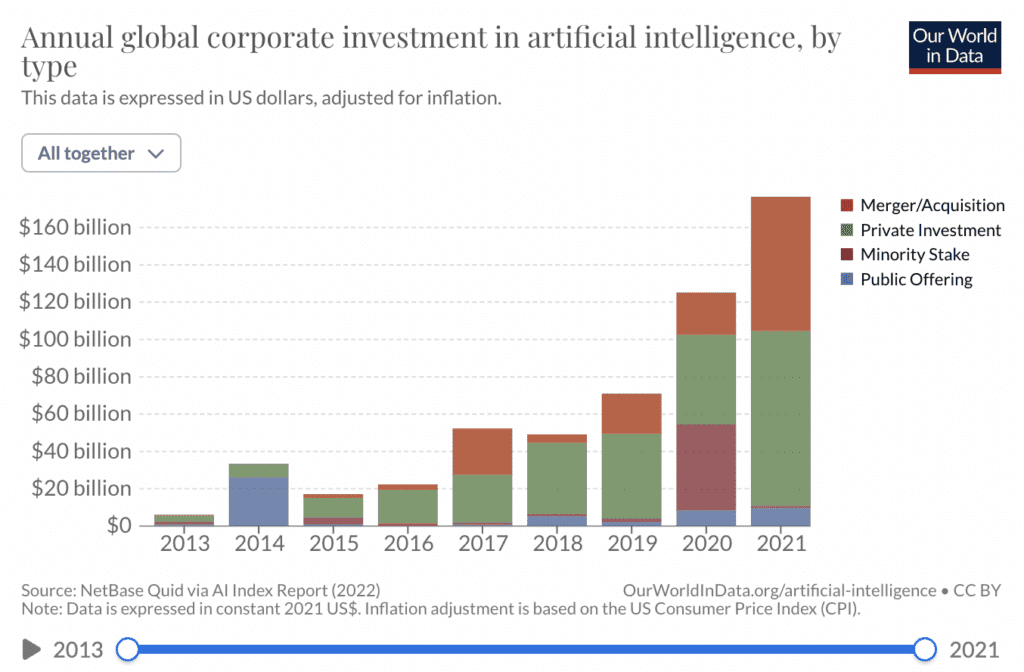

Despite the concerns, the benefits of the technology are paralleled by few, and investors have noticed. AI market size is expected to reach $407 billion by 2027 (from $87 billion in 2022), and 83% of businesses have made AI their top priority.

Generative AI to streamline lending

While AI has touched many areas of financial services, lending has seen significant innovation.

Ocrolus, a business focused on document automation and a partner to many digital lenders, has used AI since its inception in 2014. The company announced earlier this month that they were taking their usage a step further, integrating OpenAI GPT (generative pre-trained transformer) embeddings.

“It helps with contextualizing information from more challenging documents,” said Sam Bobley, Co-Founder and CEO of Ocrolus.

He explained that the company had used Optical Character Recognition (OCR) AI for several years, using technology from Google and Amazon. They had also implemented their own machine learning infrastructure to gain a high level of document recognition and streamline lenders’ document reading process for underwriting.

Related:

The combination of the three solutions had allowed Ocrolus to process documents efficiently, allowing their clients to bring loan descisioning times to a matter of hours.

In addition, the company uses human intervention to check errors in document assessment.

“The secret sauce for Oculus, one of our biggest differentiating factors is we do software, but we also have our team of Oculus quality control professionals to make sure all of the data output is perfectly clean before it goes back to the customer,” said Bobley.

Although starting with small business loans, the company had set its focus on the challenging mortgage application process. This experience allowed them to branch out to other markets, such as rental applications and personal loans.

“If you can do all of the documents in the mortgage packet, it’s very comprehensive,” he continued. “It’s allowed us to start playing in these other asset classes.”

Standardized formatting challenge

Although Ocrolus had already reduced document analysis times from days of work to a matter of minutes, Bobley explained that in some instances, the original AI systems had found it challenging to analyze documents that don’t have a standardized format.

“The hardest part of the job is contextualized information from various formats,” said Bobley. “Some of the technology that Open AI has built is superior at that contextualization effort, compared to some of the other OCR providers out there.”

“For example, pay stubs can come from hundreds of thousands of different payroll systems in the country that produce different formats. There are 5,000-10,000 banks, credit unions, and community banks.”

He said that the generative AI from OpenAI could read the documents accurately despite the differing formats, a task that may have previously needed input from a human workforce.

The result is an ability to reduce the number of erroneous documents sent for human analysis, reducing overall document analysis times even further. It also opens out the software for various alternative data sources.

“All fintech lenders are already using alternative data,” said Bobley. “I think banks and mortgage lenders are also starting to look more seriously into those data sources. We give lenders the ability to retrieve that data much faster and more accurately and deliver it directly into their own back-office credit scoring systems.”

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoAiStream. Web3 Data Intelligence. Knowledge Amplified. Access Here.

- Minting the Future w Adryenn Ashley. Access Here.

- Buy and Sell Shares in PRE-IPO Companies with PREIPO®. Access Here.

- Source: https://news.fintechnexus.com/generative-ai-enhances-alternative-data-lending-opportunity/